What are key fintech hubs across the Middle East and Africa (MEA) region?

This year The Fintech Times produced a report called Fintech: Middle East and Africa 2021 Report. A first ever, I had the privilege to main author it and concepualise the idea behind releasing a report.

The following is an except of the findings of the report after analysing 22 countries in the MEA region through three themes – wider economic development indicators, tech indicators and fintech-specific:

What were the 22 countries analysed in the MEA region? They were the following:

- Middle East and Turkey (Middle East and North Africa and Turkey): Bahrain, Israel, Jordan, Kuwait, Lebanon, Oman, Qatar, Saudi Arabia, Turkey and United Arab Emirates (UAE)

- Africa: Egypt, Ghana, Kenya, Mauritius, Morocco, Nigeria, Rwanda, Senegal, South Africa, Tanzania, Tunisia and Uganda

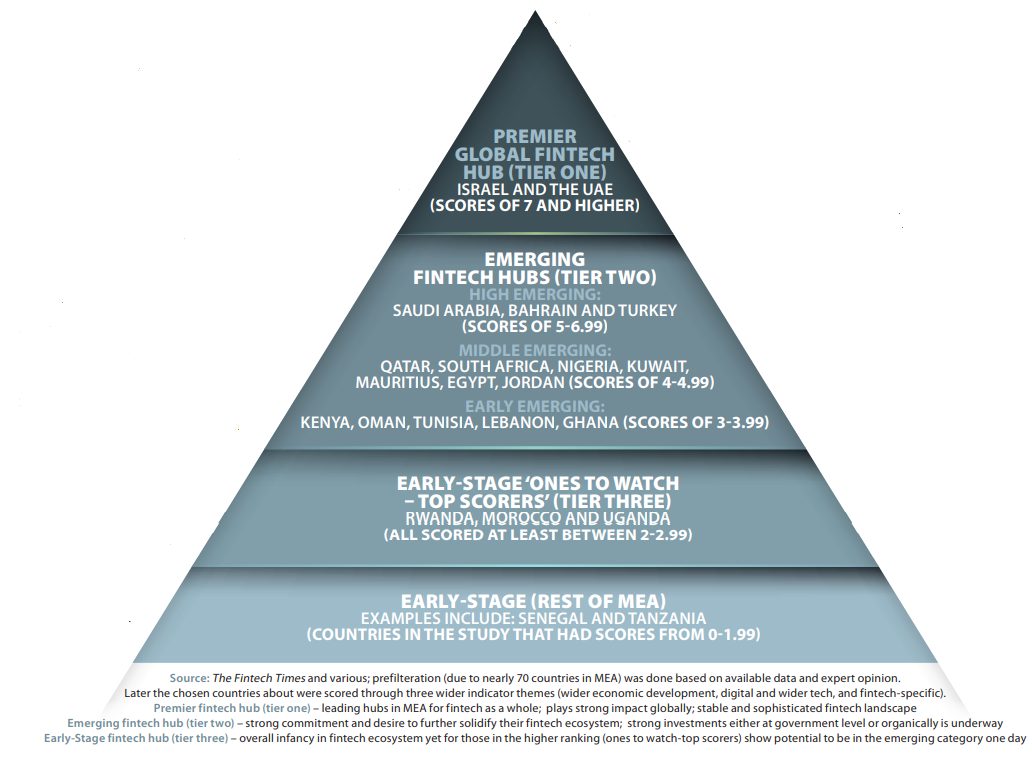

The scoring mechanism used to categorise visible fintech countries in MEA appears to endorse previous considerations. What has been helpful through this process, in particular for those not familiar at all with MEA’s fintech space, is the opportunity to provide an overview of the key player hubs in the region by categorising them into three tiers. In addition, in line with previous research studies and reports – including Middle East and North Africa (MENA) only or with Africa – a comprehensive MEA-wide analysis seems to align for the most part.

The following will reflect each of those categories as they were put in a three-tier system (tier 1 called “Premier”, tier 2 called “Emerging” and tier 3 called “Early Stage.” The following further descibes each one as taken from the report:

PREMIER FINTECH COUNTRY HUBS IN MEA

ISRAEL AND THE UAE

In the methodology for the validation research, the two countries with the overall economic development, digital and wider tech and fintech-specific categories scored a 7 or higher.

So, what exactly determines a premier global category?

It is not surprising that both nations have received this distinction. From an economic development aspect, both countries are highly-developed, as seen from high GDP per capitas all the way to high HDI indices. With respect to tech and digital as a whole, both nations are highly advanced in terms of digital infrastructure and also wider tech ecosystem. For Israel, its Startup Nation nickname showcases that. The UAE’s aspirations from its leaders have cascaded down to create an economy that has developed so fast in a short amount of time. This is clear with Dubai as well as Abu Dhabi. Particularly with the former; the city with its humble roots as a small fishing village has established itself not only as a regional hub in MEA but even a global hub contender. The growth of Dubai International Airport to be the world’s busiest international and Dubai being the number one city for regional MEA operations, of the top 500 companies globally for the two-thirds that have offices in MEA, 138 of them have established that in Dubai (beating runner up Johannesburg which had shy of 60).

With respect to fintech, both countries for the most part demonstrate their strengths. In the context of Israel, much of the data suggests that much of the strengths it has in the sector appear to be driven organically. It is the country in MEA, despite its size, with the most number of fintechs (as well as tech companies). In the UAE the strengths appear both with strong government support as well as organically. With the former, various national and Emirate-specific strategies highlight ambitions – such as aiming to be a leading global smartcity and blockchain and wider digital leader to name a few. The country has the region’s second largest number of fintechs as well as tech companies. Similar to its standing for MEA operations, in terms of MENA half of the fintech companies in the region are also in Dubai specifically.

The commitment to grow the wider financial services and economic ecosystem, where fintech plays a strong part of, can be seem visibly with the UAE’s two leading financial centres – Dubai’s Dubai International Financial Centre (DIFC) and Abu Dhabi’s Abu Dhabi Global Markets (ADGM). DIFC is the leading global financial centre in the Middle East, Africa and South Asia (MEASA) region with a vision to drive the future of finance. It is in fact the only one from MEASA in the world’s top 10 leading financial centres, ranking in at eighth place, joining other financial hubs, such as London, Singapore, Hong Kong and New York City, according to the Global Financial Centre’s Index. It is also home to DIFC FinTech Hive, a major fintech accelerator. DIFC is home to more than 50 per cent of fintech businesses in the GCC.

In terms of Israel, despite not only having the most number of both startups and fintechs in MEA, it has produced innovations that MEA (outside of its region) is still at its infancy. In other words, the Israelis have produced fintech solutions and innovations that have reached globally – companies, such as unicorns Payoneer, Rapyd, Lemonade, Fiverr and eToro, have Israeli roots. The country in the wider fintech ecosystem that encompasses the likes of cybersecurity and AI also show strong Israeli innovation. Due to the size of the country, political issues and other factors, the country has historically had to look abroad and ahead. This is why, in this context fintech and wider tech, they lead not only in MEA but are key players on a global stage.

EMERGING FINTECH HUBS:

High Emerging: Saudi Arabia, Bahrain and Turkey (Scores of 5-6.99)

Middle Emerging: Qatar, South Africa, Nigeria, Kuwait, Mauritius, Egypt, Jordan (Scores of 4-4.99)

Early Emerging: Early Emerging: Kenya, Oman, Tunisia, Lebanon, Ghana (Scores of 3-3.99)

The Emerging Fintech Hubs category consists of all the Gulf Cooperation Council (GCC) nations (minus the UAE), the four large African nations of Egypt, Nigeria, Kenya and South Africa and the small island nation of Mauritius as well as Turkey, Jordan, Tunisia and Lebanon. It is worth noting that in particular, the countries of Saudi Arabia, Bahrain, Qatar, Kuwait, South Africa and Turkey scored in the top half (scores from 5.5-6.9 – Saudi Arabia scoring the highest with Bahrain in second). The following countries that scored as emerging did so for similar themes among all of them.

For an economic development perspective, all the countries here are different in terms of their economies. However, what separated them from early-stage economies are that all the emerging fintech hub countries are either at least middle-income countries or high-income economies. It would be difficult to create an ecosystem for fintech if the wider economic development environment was not at least fairly established.

This has been reflected on their gross domestic products (GDPs) as well as various levels of other indicators used to confirm that. Some of that includes the Human Development Index (HDI) index, where all of them had fairly high scores. Another point to address with the emerging countries has been the size of some of them – particularly with countries like Nigeria whose population is 200 million people and Egypt with 100 million. Their large populations, despite it, overall put their economies at least relatively more developed compared to their other African counterparts. For the countries here that are small in terms of their size and population, notably Bahrain and Mauritius, the economic development indicators still show their strengths (high GDPs per capita – Mauritius has highlighted is one of the highest in Africa). The two countries, as seen later with the tech and digital and fintech-specific, despite their small sizes do possess strong ecosystems.

From a digital and wider tech point of view, each of the countries in this category show a reflection of their economic development advancements. For instance, often referenced together as the four in Africa from various research including that as well of The Fintech Times – Egypt, Kenya, Nigeria and South Africa, their strong showing here compared to their other fellow neighbours is evident. The four of them collectively have 85 per cent of Africa’s total fintech investments in 2019 and 82 per cent last year. Ghana also made the emerging category as well in this research.

With respect to the GCC members, their advanced economies and relatively growing tech and wider digital ecosystems justify their showing based on the research’s findings. For instance, Qatar is one of the world’s richest countries and this has allowed them to be able to build a growing tech, digital and fintech ecosystem. This is evident with their growing Qatar Fintech Hub and other infrastructure to foster it.

Neighbouring Saudi Arabia, which scored the highest here in the emerging category, is also an example of how their aspirations and advanced economies is being reflected in wider tech and fintech specifically. Being the largest economy in the GCC, the 35 million people population is undergoing massive economic development reforms and their indicators – from VC funding to even the number of fintechs – shows that.

With Bahrain, the country received the second highest score in the emerging category and it is worth noting their initiatives and aspirations. They were the first in the region to have an onshore regulatory sandbox as well as rules on open banking. In addition, being the first country to diversify their economy in the GCC has been adopted through their own strategies in the GCC. The region’s historic reliance of oil is no longer being felt and tech and fintech are key ways to change that.

To note – Turkey – with its large young and educated population and strong financial services hub of Istanbul also showcases why the country also is considered an emerging fintech hub.

In summary, the emerging fintech hubs category have all demonstrated some of the key following characteristics based on the research’s findings:

-Advanced or relatively advanced economies based on a wide range of economic indicators such as GDP and HDI

-Their wider tech scene may not be as advanced as the leaders in MEA (the premier categories – Israel and the UAE) but there are clear advancements via evident deals around tech – VC deals and the number of tech startups

-There is either a strong or in development fintech infrastructure such as with regulatory sandboxes in the respective country

-There is a sizeable number of fintechs (both as a total but divided by its population) as well as a startup scene and wider entrepreneurial activity

With Lebanon, the country that scored the lowest in the emerging category, the economy has been a historical financial hub in the Middle East region. The challenge is that the country is experiencing various economic and political challenges that, had this study been done in the past, the country most likely would have ranked higher in the study. Therefore, the result is assumed on would most likely decline from its past. For it to score better in the future in this study and maintain its emerging status it will need to see wider economic recovery, both with its challenge pre-and during COVID-19.

THE REST OF MEA: EARLY-STAGE

Early-Stage ‘ones to watch – top scorers’ (Tier-three): Rwanda, Morocco and Uganda (all scored at least between 2-2.99)

Early-Stage (rest of MEA) Examples include: Senegal and Tanzania (countries in the study that had scores from 0-1.99)

For this report as highlighted a sample of 22 countries were chosen via the prefilteration. Within the 22 countries, those that did not make the premier and emerging market ranking would be considered early stage fintech hubs. Also, those countries that did not make the prefilteration list, which are the majority of MEA countries, would also be early-stage fintech hubs.

The criteria used for this MEA report guide highlighted the importance of economic development, digital and wider tech and fintech-specific indicators. It is clear that the countries sampled that did not make the list of premier nor emerging (Uganda, Senegal, Tanzania, Rwanda, Morocco) do have the potential to do so one day. The countries were chosen based on previous data in terms of their activities in fintech. However, the findings of the research did show that the emerging and premier were decided based on the scoring mechanism that those in the early stage category did not make at this time.

For those countries that were not selected in the sample of 22, as mentioned, they would also fall in the early-stage category, albeit most likely at lower scores than the ones highlighted here.

Based on coverage from the launch of the new MEA section of The Fintech Times coupled with the research and information out in public, the countries highlighted that fell in the early-stage category have overall shown growth, interest and various degrees of commitment in growing their sectors.

For the novice in MEA, as well as those who are more familiar with the market, when presented with summarising it is clear that the economies in Africa (combination as seen from their sizes, relatively more advanced economic development and ecosystems in fintech) of Nigeria, South Africa, Kenya and Egypt made the emerging category. The only exception from the study were Tunisia and Mauritius, which the ladder despite its size is one of the richest African countries based on GDP per capita highlighted earlier in the report.

COUNTRIES TO WATCH: RWANDA, MOROCCO AND UGANDA

The countries highlighted should be commended for the work they have done in the general short time fintech has become a growing sector. For instance, the countries that scored in the higher end (2.0 to 2.99) were Rwanda, Morocco and Uganda.

Rwanda has made significant steps in boosting fintech and wider economic development, remarketing with Rwanda who many might forget had suffered its own economic and political challenges. Therefore it is remarkable to see the economy transform to be known as the ‘Singapore of Africa’. Despite both economies being much smaller than their neighbours, such as Nigeria or Kenya, their commitment to fintech and wider digital will most likely see a stronger showing for any future research done here, where its entry as an emerging hub will be a matter of not if but when. In addition, Morocco and Uganda also have a growing fintech ecosystem as well and have that opportunity to grow into emerging soon.

In summary, the section summarises based on its own research with available data from the public through its ranking based on wider economic development, digital and wider tech, and fintech-specific indicators that there are clear hubs in MEA for fintech. From the novice to the more knowledgeable of the region, the research is noting new but gives the reader a guide of the key hubs based on relevant data and filteration that incorporates elements of work previously done but putting it into a wider economic development context.

Economic development and diversification has played such a huge role and that could not be more clearer than in MEA. Whether it be through wider government strategies, such as in the GCC and in parts of Africa, to more organic growth such as in Israel, this report guide highlights that the fintech activity seen today is a direct and indirect consequence of the wider economy.

Therefore, in terms of premier fintech hubs in the region those would be both Israel and the United Arab Emirates.

In terms of emerging fintech hubs they would be Saudi Arabia, Bahrain, Qatar, Kuwait, South Africa, Turkey, Egypt, Nigeria and Kenya).

The rest of MEA would be early-stage fintech hubs but key ones to watch would be Ghana, Rwanda and Lebanon.

To read the full report click here.