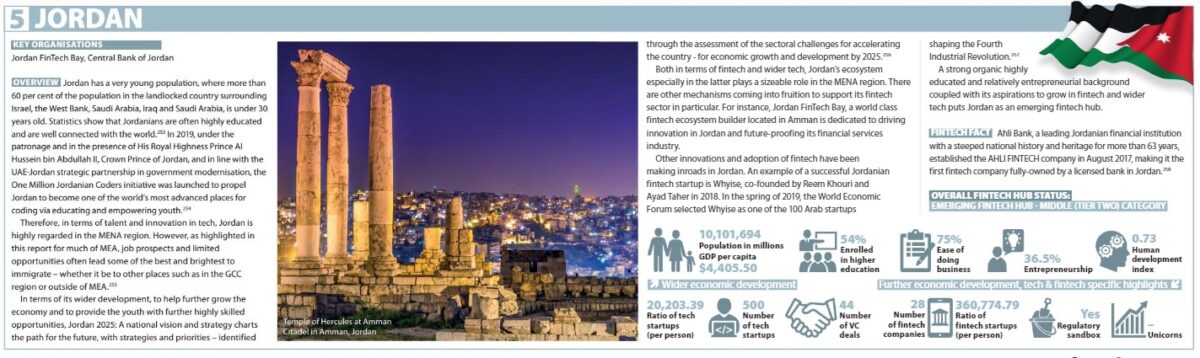

The Middle East and Africa’s (MEA’s) fintech sector is booming, as countries across the region are developing their digital ecosystems, providing new opportunities for startups and existing businesses. One country that has seen success in particular, is the Kingdom of Jordan.

In the previous The Fintech Times Fintech: Middle East and Africa 2021 Report, we reported that Jordan, similar to much of the MEA region, has a very young population, where around 60 per cent of it is under 30 years old. Statistics have shown that Jordanians are often highly educated and are well connected with the world. Nevertheless, as is the case in other parts of MEA too, may have had to immigrate to seek better opportunities, as estimations suggest10 per cent of its citizens are abroad.

To improve its wider economic development, the Kingdom came up with Jordan 2025: A national vision and strategy. Through the assessment of sectoral challenges identified, the strategy provides initiatives amongst other things that will help the country accelerate its economic growth and development by 2025.

The Central Bank of Jordan (CBJ)’s National Financial Inclusion Strategy 2018-2020 also aimed to “build on a set of priority policy areas, three of which form the core sectoral pillars: microfinance; digital financial services; and small and medium-sized enterprise finance. Four areas are considered as cross-cutting enablers that facilitate the development of industries and make them more robust: Financial technology; financial consumer protection and financial capabilities; data and research; and laws, regulations and instructions.”

According to the same report, only 33 per cent of adults in Jordan, and 27 per cent of women, were financially included in terms of account ownership. Even though it had a very high rate when compared to its Middle East and North Africa (MENA) peers, it was and still is considered low in comparison to other nations with similar income levels. Therefore, having an educated population, coupled with relatively strong entrepreneurship and startup scene, presents an opportunity for the Kingdom of Jodan.

Earlier this year, Cairo Amman Bank built the neobank LINC. This new digital ‘bank for you’ offers a full suite of financial services like debit, credit, prepaid cards, international money transfers – to name a few of its perks.

Partnerships are also happening between banks and fintechs. For example, Arab Bank has two initiatives that are focused on fintech collaboration, AB iHub and AB Accelerator. AB iHub builds rapid prototypes and uses fintech ecosystem collaborations and bootcamps to work directly with fintechs and individuals in the ecosystem. The AB Accelerator programme focuses on the adoption of emerging fintech technologies into Arab Bank’s infrastructure and network – as highlighted in a report by KPMG.

Another initiative highlighted by KPMG is the ISSF (Innovative Startup and SMEs Fund), which launched with a $100million fund, is focused in part on the fintech industry. Initiatives such as this help build the startup ecosystem and spur investment from the private sector. Success has been seen in the last year as the ISSF had a $400,000 joint fundraising between the company itself, Jordan Ahli Bank and startup, Whyise.

The country’s central bank, CBJ, like many highlighted in the Middle East and Africa (MEA), has established a regulatory sandbox. According to the CBJ, it “targets mainly all innovative financial solutions that include money transfers, and enhancing security, efficiency, and competition in providing such services. The Fintech Sandbox will include: electronic payments and money transfers, including cross-border remittances; saving, financing and credit services; consumer protection services, tracing and resolving complaints; mitigating risks and financial fraud detection services; building a digital financial identity and a credit history for clients; innovative digital verification for clients; crypto-currencies (not virtual), blockchain and DLT platforms; conventional financial and banking services but in an innovative technological form; conventional financial and banking services that enhance digital; financial inclusion, and serve non-financial sectors; regtech services; and any other regulatory or supervisory services that achieve the objectives of the fintech sandbox.”

According to Statista, the market’s largest segment will be digital payments with a total transaction value of $6.3billion this year. To note, a big part of Jordan’s fintech ecosystem development was the CBJ creating the Jordan Payments and Clearing Company (JoPaCC), which helps develop digital payment systems and invest in innovative technologies.

It is worth noting that Jordan hosts 760,000 refugees and asylum seekers registered with UNHCR. Of those, some 670,000 are from Syria, making Jordan the number two host of Syrian refugees per capita globally behind Lebanon. Many are financially excluded due to their circumstances.

In Jordan, as highlighted by Tufts University, the government has promoted the use of electronic financial accounts through mobile wallets. These ‘m-wallets’ are digital reservoirs on mobile phones where users can store money that they can later release as payments, remittances, or cash withdrawals. Despite its priority in the inclusion strategy, m-wallets weren’t really mainstream until the 2020 pandemic came around and made digital vital for everyone, including in Jordanians.

The CBJ took prompt measures to allow online registration and electronic know your customer (KYC) verification for m-wallets. This included CBJ partnering with the National Aid Fund (NAF) and Social Security Corporation (SSC) to distribute aid to vulnerable Jordanians through m-wallets. From March to July 2020 Jordan saw a 40 per cent increase in the number of registered wallets, while by May last year saw one million wallets registered.

With regards to refugees, there have been pilots to use digital payments, which include humanitarian transfers, to disburse cash to refugees through m-wallets. Some of those include a pilot by GIZ and Zain Cash to distribute payments under the ‘Cash for Work’ programme has been implemented in Fifa, Azraq, Dibeen, Ajloun, and Yarmouk. Under 2,000 (1,948) workers (vulnerable Jordanians and refugees) benefited from the usage of m-wallets. Jordan’s importance in being a home for refugees – historically mainly Palestinians and recently mainly Syrians – presents further opportunities where fintech can help the financially excluded refugees.

The Kingdom of Jordan presents an opportunity to further grow its wider digital economy and fintech plays and will continue to do so in that environment.