Kate Goldfintch, Editor at The Fintech Times.

Exponential growth and a complete transformation of the way future projects will acquire funding, is a key trend for wealth management and investment markets. We see numerous projects raising money through tokenisation, and cryptocurrencies; thereby allowing global access. The Fintech Times observes how fintech is shaping the asset & wealth management industries.

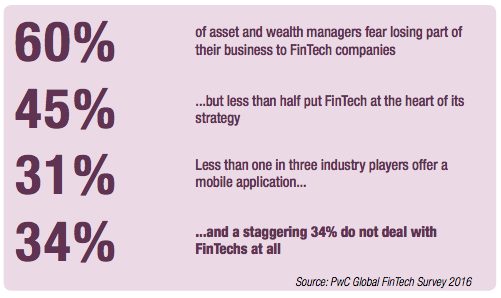

The majority of asset and wealth managers or AWMs (60%) fear losing part of their business to fintech companies, according to the Global Fintech Survey-2016 by PWC “Beyond automated advice. How fintech is shaping asset & wealth management”. The main fintech-related concern of asset and wealth managers is pressure on margins, but many incumbents underestimate the disruptive potential of new entrants, believing they pose no risk. Over a third of asset and wealth managers (34%) do not engage with fintech companies at all. 69% of asset and wealth managers who do engage with fintechs expect to see their costs reduced as a result.

ICOs are disrupting the angel investor model; opening an opportunity to respond to many of the funding challenges faced by start-ups and scale-ups. “Robo-advisors” create an opportunity for asset managers to target the affluent who are looking for cheaper alternatives for advice on how to manage their assets.

AWMs should watch fintech companies closely and adopt responsive digital strategies. Otherwise, they face losing their business to new entrants.

Asset and wealth management evolution

After leading the way with technology in the 1980s, AWMs have become dismissive of technological innovations and disruptions to their industry. During the emergence of online brokerages, wire houses gave the upstarts pejorative titles, such as “discount brokers”, holding the belief that these new business models would fail to take off, and the risk they posed to businesses was low. In reality, these new competitors commoditised trade execution, significantly dropping the price that companies can charge per trade.

“Eventually, they introduced new pricing models by splitting advice from transactions – full service brokers started to charge on a fee per asset under management (AuM) basis versus fees per trade. History could repeat itself again with the ongoing disruption caused by fintech companies. Much like online brokerages, ‘roboadvisors’ have been disparaged as less valuable than human professional wealth advisors, and so far have been focusing mainly on low balance accounts. But the innovations under the umbrella of ‘robo-advisors’ are becoming more sophisticated and, thus, enable advisors to service higher net worth accounts. Technological revolution In fact, ‘robo-advisors’ create an opportunity for asset managers to target those who are looking for cheaper ways to manage their assets. Participants in PwC’s global fintech survey view asset and wealth management (AWM) as the third most likely field to be disrupted (35%), while 60% of asset and wealth managers think that at least part of their business could be threatened by – lower than most other financial sectors. By being too complacent, investing mainly in self-serving automation, and ignoring the imminent technological revolution, asset and wealth managers may lose touch with their core clients. Additionally, they could miss the opportunity, already tapped by fintechst. Keeping abreast with how fintech is reshaping the industry seems like the most reasonable way forward.

“New accelerated online platforms and applications buy levitra pakistan improve the retail customer experience by providing bespoke but affordable services to help investors set their investment goals, choose the right product or service and manage their investment portfolios. A secondary by-product of automated customer analysis is a lower cost of customer onboarding, conversion and funding. This creates a challenge for AWMs who have struggled for years to figure out how to create profitable relationships with clients in possession of fewer total assets. Some AWMs, as well as retail banks and insurers, have already reacted by acquiring such platforms or by building up their automated advisory solutions,” researchers clarify.

The innovations under the umbrella of ‘roboadvisors’ are becoming more sophisticated, and many start-ups are pivoting to enable a digital experience. Those who are ready to embrace the fintech disruption could go a step further and become firstmovers in incorporating broader multi-source data sets, and forming a more holistic view of the customers. In particular, AWMs could become data custodians as they are already deemed highly trustworthy data collectors. By leveraging the entrusted data, they could offer comprehensive solutions that address client needs, based on life goals and expectations.

While defending, and improving, the core elements of their operations using automation and sophisticated analysis, AWMs have also noted the emergence of alternative business models and technologies. These have, for the time being, a lower propensity to elicit a response, although this might soon change.

Alternative business models

Innovative business models, such as marketplaces and investor networks, are changing the way investments are made. E.g. crowdsourcing platforms are encouraging users to benefit from the collective wisdom of the communities they nurture. Users exchange insights, information, and even investment algorithms to leverage collective investing intelligence. “These innovative business models aim to create value through connections among a variety of a platform’s users: investors, financial advisors and asset managers,” PwC research explains.

Distributed Ledger Technology (DLT)may also affect AWMs and the whole industry. By using DLT, the need for reconciliation of proprietary databases is eliminated. Embedding business logic in the code of a smart contract could also impact the AWM value chain in terms of augmenting, streamlining or possibly completely reinventing current processes. The use of the so called Distributed Autonomous Organisations (DAO), if properly implemented, could lead to decentralised and autonomous investment vehicles that operate through blockchain technology and smart contracts.

Machine learning (ML) is also transforming asset and wealth management. ML is enabling computers to identify patterns in market behaviour and analyse transactions almost in real time. “This, in turn, is reducing the asymmetry of information between small and large financial institutions and investors. Alternative data pools are also increasing AWMs’ usage of accurate predictive analysis supported by innovative data and opinion mining, imagery analytics, machine learning and artificial intelligence techniques,” PwC analytics emphasise.

How to “win” in a new paradigm

In conclusion, the asset and wealth management industries are on the cusp of huge change. Incumbents and fintechs have to cooperate to ‘win’ in the growing new paradigm. Traditional players have to be more open towards engaging with the new entrants. AWMs who want to win in the redesigned market must find the right mix of technological improvements, coupled with an adequate pricing structure.