The following gives an overview of Kingdom of Bahrain and its relationship with both fintech and wider financial services and digital.

Bahrain has over 120 fintechs but the majority are within payments and crypto. This is according to Bahrain Fintech Bay’s ‘Fintech Ecosystem 2022’ report. Furthermore, the report highlights other facts – that the Central Bank of Bahrain (CBB) has been introducing several new regulatory reforms and policies including crypto-assets, digital financial advice, crowdfunding, open banking and the e-KYC framework.

The ecosystem also boasts over 19 incubators and accelerators in the Kingdom. In terms of government support beyond just legislation, which in the Middle East and Africa (MEA) as a whole Bahrain has been leading much in terms of a more regulated approach on areas like open banking, the government can be seen doing this with investment.

There are almost eight investing entities in the Island nation that are actively investing in fintechs.

Key organisations that help foster the wider fintech and Bahraini ecosystem include:

- Bahrain Economic Development Board (EDB) – the country’s investment promotion agency with overall responsibility for attracting investment into the Kingdom and supporting initiatives that enhance the investment climate.

- Bahrain Fintech Bay – the first and largest fintech hub in the Middle East, which is connected through a global consortium of fintech bays.

- Al Waha Fund of Funds – a $100million venture capital fund that provides funding access to Bahrain’s startup industry.

- Women in Fintech Bahrain (WIFBH), an initiative to raise awareness of women’s role in fintech in Bahrain, cultivate new industry opportunities in Bahrain, and contribute to the development of an inclusive and supportive fintech ecosystem.

- Central Bank of Bahrain (CBB) – the Kingdom’s central bank.

Despite the Kingdom’s small size (it is only a mere 765.3 square kilometres), as mentioned due to its lead in the MEA region as a whole with respect to being business and expat-friendly, coupled with its pro-regulatory approach that has resulted in an attractive fintech friendly regulatory framework it is appealing for investors and the sector as a whole.

An example of this has been being a pioneer in the MEA region with its regulatory sandbox, one of the first in the Middle East and North Africa (MENA) region following economic free zones Abu Dhabi Global Market (ADGM) and Dubai International Financial Centre (DIFC); Bahrain’s was introduced by the CBB and was the first on-shore.

As of September 2021, there are 25 fintech companies in the sandbox, with over three-fourths coming from MENA. The largest areas of fintech they represent are buy now pay later (BNPL) at 16 per cent of total companies, robo-advisory at also 16 per cent and crypto services (ATM, tokenisation) at 12 per cent.

Examples of those companies include the likes of crypto platform Rain, trading platform CoinMENA, and digital banking platform provider Aion Digital and open banking platform Tarabut Gateway.

Another example has been its championing of open banking in arguably not just the Gulf region but MEA as a whole. In 2018 they issued open banking rules and then the framework on its governance and sharing of data followed in 2020.

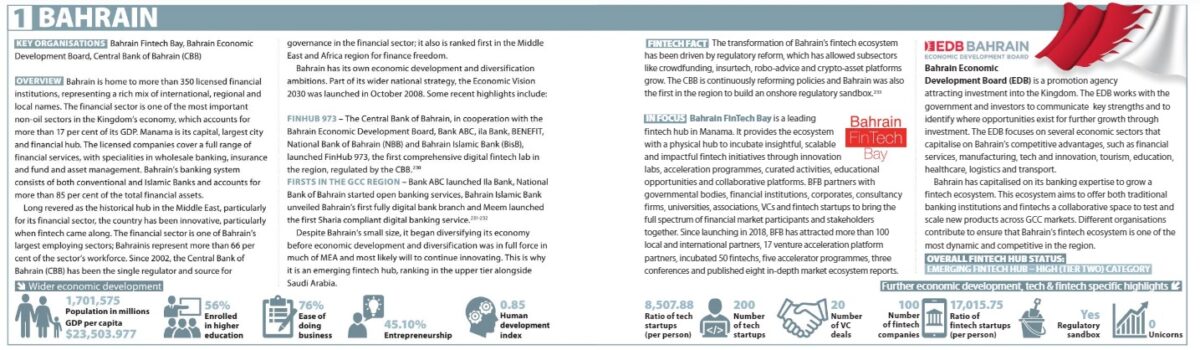

Also, as highlighted in the Fintech: Middle East and Africa 2021 edition, the Kingdom has been a historical financial services hub. It is home to almost 400 licenced financial institutions, representing a mix of international, regional and local names. Representing one of its most important non-oil sectors, it accounts for over 17 per cent of its gross domestic product (GDP).

The financial sector is also one of Bahrain’s largest employing sectors; Bahrainis represent over 66 per cent of the sector’s workforce. Other interesting facts are that, since 2002, the CBB has been the single regulator and source for governance in the financial sector; it also is ranked first in the MENA region for financial freedom.

In terms of fintech adoption and/or disruption, the Fintech Bay reports that retail banking had the highest adoption and/or disruption at 68 per cent, which was followed in second place by telecommunications at 41 per cent and third place at 40 per cent with corporate banking.

Despite the challenges of Covid-19, Bahrain’s vision and the 2020-present pandemic further solidified the need and growth for fintech and wider digital.

According to figures from the CBB last year, there were more than 11.3 million digital transactions in Bahrain during the month of August, valued at $743.7million. The value of e-commerce and point-of-sale (PoS) payments rose by 50 per cent in August when compared to the same month last year.

The data also shows how there were more than 53 million digital payments in the first half of last year. Bahrain’s national electronic wallet, BenefitPay, announced a 785 per cent increase in the number of remittances through its Fawri+ service (an online payment service introduced under the Electronic Funds Transfer System) in 2020 – exceeding $5million.

Innovations and other collaborations have launched as well. This includes, FinHub 973, launched by the CBB, is the region’s first cross-border, digital innovation platform that connects and facilitates collaboration between financial institutions and fintechs under the supervision of the central bank.

Also, Batelco (the telecommunications company in the Kingdom) became the first teleco in the Gulf Cooperation Council (GCC) region to receive a licence for open banking last year.

On a final note, much of what has driven this, as written before in the previous references including my report, has been its wider economic development and diversification strategy called Bahrain Economic Vision 2030 – where it sees a future that will be not only less oil-reliant but one that will further promote innovation, economic diversification with highly skilled sectors like fintech, entrepreneurship and overall better quality of life.

Bahrain, despite being small, has had a large vision, success and aspiration that sees fintech and innovation as a part of that.