What have been some of the developments in the fintech and wider digital ecosystems in the East African nation of Tanzania?

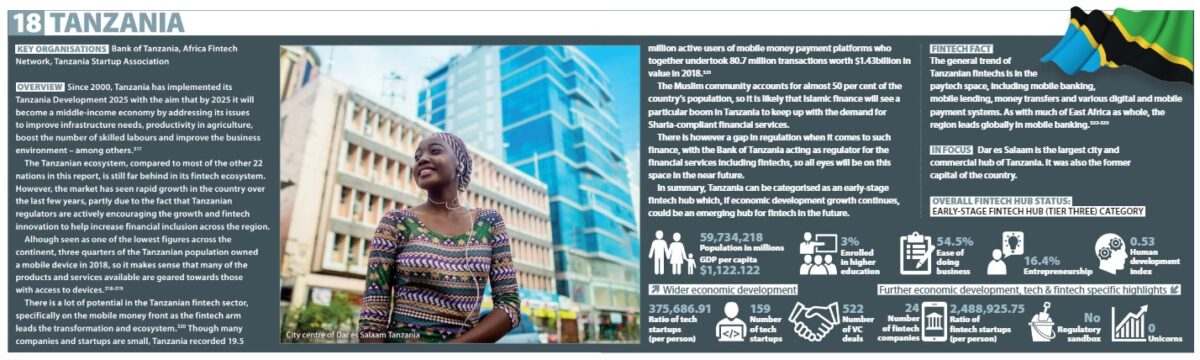

As highlighted in my previous The Fintech Times Fintech: Middle East and Africa 2021 Report, Tanzania has been implementing its economic development strategy, Tanzania Development 2025, since the start of the new millennium in 2000. The aim of this is that by 2025 Tanzania will have become a middle-income economy: addressing its issues to improve infrastructure needs, productivity in agriculture, boost the number of skilled labours and improve the business environment – to name a few.

According to a study from the United Nations Capital Development Fund (UNCDF) last year, Tanzania’s fintech landscape has grown and changed positively due to regulatory reforms in the payment sector launch of government policies and initiatives focusing on information and communication technology (ICT). This was evident in 2015, when the Tanzanian government established the Information and Communications Technologies Commission (ICT Commission), which has a mandate of coordinating and facilitating the implementation of national ICT initiatives. Also, the government has an MoU with ecosystem facilitator Financial Sector Deepening Trust (FSDT), where the FSDT can provide financial and technical support to the financial sector, while the government provides support to the sector with legal and regulatory frameworks.

This has helped Tanzania to catch up and advance digitally when fintech services at the time were limited mainly to airtime purchases, cash deposits, and money transfers and withdrawals. To note, in terms of its fintech subsectors, out of the 33 estimated fintechs in Tanzania, lending/financing and payments/remittances were the two most popular at 14 and 10 fintechs respectively. In third place was savings with five; fourth place, insurance with four fintechs; enabling processes and technologies in fifth with three fintechs, and finally personal finance with two fintechs.

Like the rest of its fellow East African peers, Tanzania has seen mobile money help bring about financial inclusion to much of its population. The percentage of Tanzanian citizens using formal financial services grew from only 16 per cent in 2009 to 65 per cent in 2017. Since June 2021, Tanzania has had over 33 million (33.2) mobile money accounts opened – all according to the Global System for Mobile Communications (GSMA).

As of last year, there are currently six mobile network operators (MNOs) in Tanzania, with many partnering with financial service providers that enable peer-to-peer (P2P) payments via mobile wallets and digital banking services. Some of these players include M-Pesa from Safaricom, Tigo Pesa from Tigo, and Airtel Money.

In July last year, the country introduced a new tax on mobile money transfer and withdrawal transactions (minus merchant, business and government payment transactions). This levy is in addition to their VAT of 18 per cent and excise duty on mobile money transfer and withdrawal fees of 10 per cent.

From a report from the GSMA analysing the impact of this, it stated that until June 2021 taxes on mobile money fees were 23 per cent of total transfer costs but by July and August last year that became 60 percent. To put this into perspective, from July last year with the levy, Tanzania’s average transaction became three times higher than the average fee of East Africa (previously the country had been in line with the average for the region). This saw dramatic declines in transactions from June to September last year such as with P2P transactions that went down 38 per cent for instance. However, by the end of the year mobile money appeared to slowly have recovered and increased again following the levy “shock.” Nonetheless, it is estimated that the market contracted 12 per cent as a result of this and the future growth of it will be less than pre-levy.

It could present a problem, if too expensive, as people in Tanzania may resort to cash again, which would ruin any digital gains mobile money has had in the country.

Another problem has been the lack of regulations, including its lack of a regulatory sandbox, as they have been unclear for many of the fintechs and wider tech companies in the country.

A further challenge for startups and fintechs has been a lack of funding and/or mentorship. For the estimated 33 fintechs in the country, only 36 per cent of them have managed to secure seed funding or growth financing, while 35 per cent are bootstrapping via friends and family members.

Nevertheless, it appears more is happening and the ecosystem is further advancing. At the end of last year, for example, the Bank of Tanzania announced it was in the process of developing a central bank digital currency (CBDC) – assuming it will be the digital version of its current currency the Tanzanian Shilling or e-Shilling.

Despite the fintech ecosystem being more infant than its other Middle East and Africa (MEA) peers, there have been organic successes. Earlier this year, it was announced that Tanzanian fintech NALA, a cross-border payments company, was able to raise $10million seed.

Tanzania has been one of the African continent’s fastest growing economies, with a seven per cent average annual growth in its national gross domestic product (GDP) since 2000. It is also one of the top 10 largest countries in Africa by population, showing that its transition from a low-middle to a middle-income economy (and beyond) will present opportunities and inclusion for all its people.

The country compared to the others still lags behind with respect to its fintech and wider tech ecosystem. Nevertheless, it has been playing catching up and has achieved what it could thus far. It will be important for the growth of the ecosystem that further incentives and initiatives for fintech take place, as well as partnerships and further collaborations and expansion of the ecosystem – education and trainings, accelerators/incubators, to name a few.

On a final note, in the wider tech ecosystem, there are organic examples. One of which is Silicon Dar, an initiative to promote the new technology district of Dar es Salaam, which according to its website the area is home of the several innovation hubs, telecom companies, college of ICT of University of Dar es Salaam, data centres, Commission For Science and Technology, tech startup companies and business incubators.

Tanzania’s growing economy can have fintech play a strong part of it in the future, as it already has made an impact in the lives of many Tanzanians.