Q&A with NIELS TURFBOER, managing director of alternative lender, Spotcap, UK and Benelux

What is Spotcap?

Spotcap is a multinational fintech lender that issues unsecured credit lines and loans to small and medium size businesses. We lend from our balance sheet and use tried and tested principles to assess credit. What sets us apart is our use of new technology. Artificial intelligence and predictive analytics are part of our in-house developed approach. They help give applicants a swift and straightforward user experience, allowing them to focus on what matters — their business.

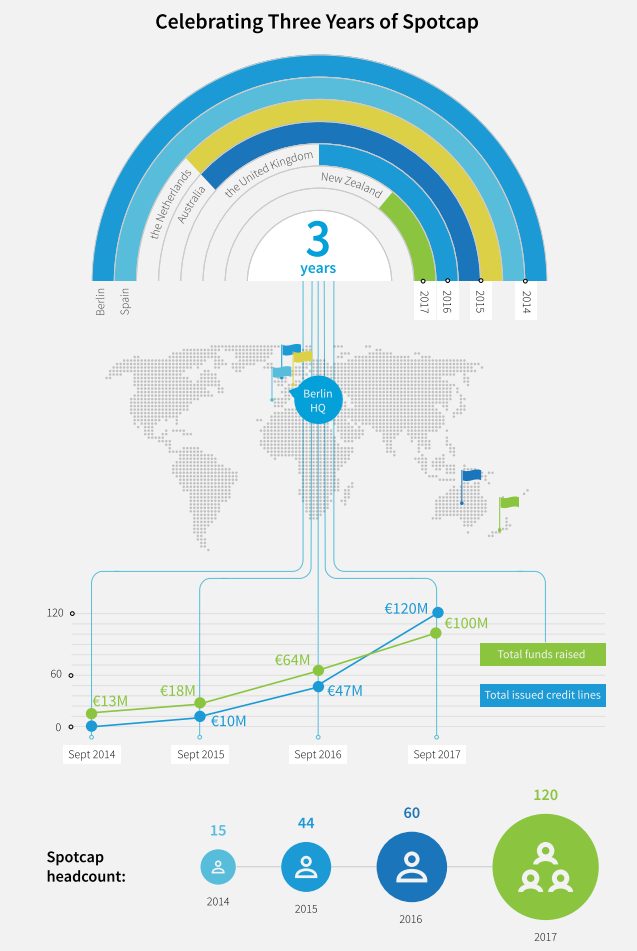

Spotcap was founded in 2014 by an experienced team with years at leading European financial institutions. Our headquarters are located in Berlin and we operate in the Netherlands, the UK, Spain, Australia and New Zealand.

What problem do you solve?

Let’s look at the UK. There are 5.5 million private sector businesses there. More than 99 percent of these are small or medium size. Despite a combined annual turnover of £1.8 trillion these businesses often face difficulties finding financing to meet their needs. Many of these firms are looking for unsecured financing. The government has tried, in numerous ways, to make it easier for them. Its Enterprise Finance Mind the Funding Gap Guarantee (EFG) scheme was set up in 2009 to help businesses which did not have sufficient security to access funds.

Spotcap addresses this need. It offers businesses that have been operational for at least two years access to unsecured funds, from £10k to £300k. There is no cost or commitment to apply and set up our credit line. Repayments start once a drawdown is made.

Who has benefited from a Spotcap loan?

We have helped thousands of businesses with their financing needs. Common uses include: managing cashflows, bridging receivables and buying inventory. In the Netherlands, we recently helped a business specialising in home decorations to grow from two founders to 35 employees in just one year.

In the UK, we just issued a 300k credit line to a construction company in South Wales. The company was expecting a new investment but due to rapid growth there was a funding gap of a few months. Spotcap was able to step in and bridge this gap until the new funds were made available.

How do you work with partners?

Collaboration and partnerships have always been part of our strategy on both a tactical and strategic level.

To date a significant portion of our loan book is attributed to business owners who came to us through their financial advisor, accountant or broker. It’s fair to say they have played a strong hand in our success. Earlier this year, Spotcap announced a partnership with Heartland, New Zealand’s only NZX-listed bank. The partnership began with the bank investing £13 million (A$20M) of debt in the business and has evolved into a strategic, mutually beneficial relationship. Finstar Financial Group is another of our strategic investors. All parties bring expertise, experience and contacts to the table. We’re now exploring new ways to provide our technological expertise to established players and to work with them to explore new markets and underserved business communities.

The alternative lending industry hasn’t been through a credit downturn, what safeguards do you have in place to ensure Spotcap would make it through one?

While current conditions may be “as good as it gets”, a downturn will come eventually. The lenders that will end up ok will be those who have taken a considered and long-term approach to how they are building their business. Spotcap is run by a team that have decades of experience at traditional financial institutions. We have been through credit cycles and are aware of systematic risks. Together we have built Spotcap to withstand macroeconomic conditions and industry trends. Moreover, as a balance sheet lender, we are incentivised to take responsibility for our credit decisions.

How do you evaluaate the upcoming changes such as GDPR and Open Banking/PSD2?

These changes make an important statement about data ownership — placing it firmly within the hands of the consumer. PSD2 will enable trusted third parties, with permission from consumers, to leverage banking data to provide an enhanced consumer experience. It will also make it easier for fintech businesses to enter the market, increasing innovation and competition.

The global data protection regulations will also push businesses to ensure data is secure. The ‘Privacy by Design’ requirements laid out in new global data protection regulation (GDPR) set an obligation for businesses to consider data protection as they begin to build products, creating a win-win situation for consumers and businesses.

Where to next?

In the next 12 months, we will continue to work with our intermediary partner network to increase our market share in each of our five countries. We will also continue to build strategic relationships and lend directly to small business companies — all with a focus on responsible lending based on sound financial assessment. We believe good things will come of it.