Simon GIlbert, Founder and Managing Director at Elmore Insurance Brokers Limited, specialists in FinTech Insurance

Hi Simon, thank you for your time in this busy part of the year. We have learned a lot about PSD2 & GDPR in the last months, what impact does that have on the Insurance a FinTech needs?

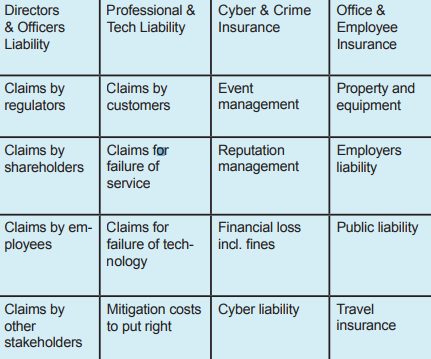

My pleasure, I am very passionate about this topic. The beauty of the FinTech industry is that they develop solutions in a matter of weeks, which used to take firms decades to develop. Many FinTech companies rely on networks, systems, data, cloud technology, and outsourced service providers to scale and build their incredible technology. This exposes a FinTech to different types of risks, which the insurance industry has addressed with FinTech Insurance.

Well, that’s interesting, what’s different about FINTECH INSURANCE?

Providing or facilitating any type of financial services means professional indemnity insurance (PII) is a regulatory required insurance (as per PSD2), whilst directors’ and officers’ insurance is key for attracting and retaining management and ensuring their personal assets are protected. The difference vs traditional companies comes into play as the majority of FinTechs will be pushing the boundaries of innovation and will have a combination of technology, money, crypto currency and personal data at their core, protection against cyber risks and cyber-crime risks is an essential part of FinTech Insurance.

What would you recommend to any FinTech in regards to managing their insurance policy?

High growth fintech companies are typically short of resources, therefore the speed and efficiency with which claims are handled and settled is critical, so that, in case of a claim, the FinTech can focus on growing their business. Three important considerations should be made before purchasing a fintech insurance policy:

1. Understand the policy exclusions and what is not covered by the policy

2. Find out which experts are provided by the policy to assist at the time of a claim

3. Ensure that the broker and insurer you are dealing with understands your

business

What’s the benefit of risk management to any FinTech and who would you recommend to use risk management solutions?

Every company is subject to internal and external risks and the first step is to be honest about them and identify them within a business. The goal then is to reduce them by following best practice controls and processes and ideally certifying these to industry recognised levels. This will then be a good argument and evidence to improve insurance coverage and premiums, while improving the overall governance and operational control of a successful FinTech.

Last question, please share with us how Elmore is helping the FinTech industry?

I started Elmore 2 years and apart from the cyber security and GDPR risks which needs cyber insurance we have been doing a lot of work recently on PSD2 and the professional indemnity insurance. About half of our clients now are FinTechs and they value to be dealing with an insurance start-up that not only understands their challenges, but also shares a similar culture.