The explosive growth of the FinTech industry has facilitated efficient, cost effective ways of transferring money across international borders. FinTech enterprises have picked up the slack where banks and traditional financial institutions have failed. The un-banked and under-banked sectors now have a voice with FinTech. There are many reasons why these innovative companies have experienced explosive growth, notably the dramatically reduced fees, no middlemen, and lower spreads than banks.

Many of these FinTech companies have stockpiles of cash all over the world, making it much easier to simply pay out in each country. Banks rely on old school methods of purchasing currency and then converting that currency into foreign currency. When transferring money abroad with FinTech enterprises, these companies have established operations in foreign countries where the equivalent figure is simply paid out in the receiver’s currency on the other side.

This reduces transactions processing fees, currency exchange fees, brokerage fees, and the high spreads that banks levy on Forex etc. FinTech companies have adopted greater transparency in their fee structures than banks – contributing to their increased popularity among customers. You will always know how much you are paying for your Forex, unlike with banks where quoted rates from Thomson Reuters differ dramatically from the actual rates that you pay when purchasing and sending currency abroad.

How Much Money Is Transferred Abroad on an Annual Basis?

Cross-border funds transfers between banks number in the trillions of dollars. Consider that back in 2005, the Fedwire processed 528,000 transactions with a value of $2.1 trillion. The value of cross-border funds via SWIFT transfers was valued at $5 trillion per day back in 2004. Clearly this multi-trillion dollar industry ranks among the largest of all the ongoing financial transactions. The Bank for International Settlements (BIS) is responsible for the efficient circulation of money around the world. It handles global money transfer in debit cards, document credits, credit cards, credit transfers, direct debits etc.

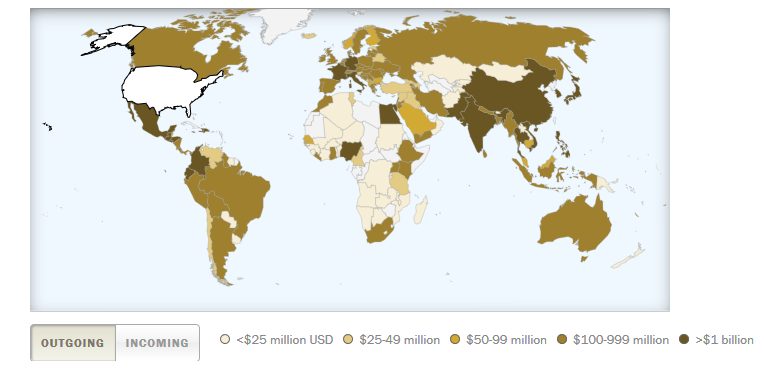

According to the Pew Research Center, remittance flows in 2015 amounted to $133,552,000,000 from the US to other countries alone. Worldwide, it was estimated that $582 billion was sent by migrant workers to their home countries. The countries with the highest receiving remittances include Guatemala, Nigeria, El Salvador, Dominican Republic, Honduras, South Korea, Germany, France, Jamaica, Japan, Colombia, Thailand, Italy, Haiti, and Lebanon. Most of the remittances flow from high income countries to low income countries, i.e. from developed economies to developing economies. However, many people in developed countries receive remittances from abroad too.

The Impact of International Money Transfers

International money transfers increase the velocity flow of money between countries, and establish balance between low income countries and wealthier countries. By eliminating banks from the equation, the actual cost savings amount to billions of dollars every year. FinTech companies have capitalized on the shortcomings of banks, and people are saving more of their own money and banking more of their own money than ever before. Less fees, commissions and hidden charges are being paid through non-bank entities, and the comfort, convenience, and cost effectiveness of FinTech money transfer options has already resulted in significant cost savings.

Given that the spread at FinTech companies is far less than with banks, the rate being paid for Forex is much closer to the market rates. Information provided by Money Transfer Comparison indicates just how much customers are saving by using established and trusted non-bank entities for money transfer purposes. For example, the leading FinTech companies (OFX, Transferwise, FC Exchange, Halo Financial et al) are officially regulated by monetary authority such as the FCA (Financial Conduct Authority), all money transfers are tracked and recorded, and they all feature favourably with objective ratings sites such as TrustPilot.

Why Fintech Global Transfers Makes Sense

It is in customers best interests to compare banks to non-bank entities to see how greater efficiency, and cost savings can be enjoyed. The biggest benefits include no fees and commissions, better Forex rates, and optimized payments systems. Plus, there is often guidance on how best to exchange currencies and at the most opportune times. These services are best suited to individuals, expats, SMEs, overseas property buyers, for small, medium and large transfers. The personal assistance provided by non-bank at FinTech companies surpasses those of banks, making these a highly sought-after option for clients.