Starling Bank today published a trading update for the three months to 31 October and announced that it has become the first of the new breed of digital banks to break even, thanks to strong momentum in customer accounts and revenues, coupled with a stable opex base.

With nearly 1.8 million accounts, c.£4 billion in deposits and c.£1.5 billion of lending, Starling expects to be profitable on a monthly basis going forward as it continues to grow and gears up to scale across Europe.

In CEO Anne Boden’s latest blog she outlines how, when pitching the prospect of a technology-led bank and a profitable business, she didn’t even have a banking license. Fast forward five years and Starling has won Best British Bank at the British Bank Awards for the past three years. Anne recently documented her journey as founder in her new book, Banking On It: How I Disrupted an Industry, released earlier in November.

Yet when the pandemic hit in 2020, Starling was quick to sign up as a lender for the government-backed Bounce Back Loan Scheme (BBLS), which offers support for small and medium-sized businesses.

As of the end of October 2020, Starling had c.£1.5bn of lending on the balance sheet, with £86m being retail customer lending and the remaining £1,379m being SME lending, the majority of which is made up of BBLS.

In an exclusive interview with The Fintech Times, CEO Anne Boden explains just why the digital bank decided to join the scheme.

At what point in 2020 did Starling realise they wanted to be involved in the BBLS?

Being there for our customers, has always been our priority so we applied to become accredited as a BBLS lender as soon as the scheme was introduced. We had to make sure that our customers had access to this lending.

The decision wasn’t just made by Anne alone as we work as a team at Starling. The entire executive team and the board were involved.

Once you decided to press go, how did you start?

We did what we always do. We gathered the whole team together, rolled our sleeves up and built the entire system ourselves, using our own engineers, lending and other in-house expertise. The team literally worked round the clock to get it ready. We were accredited on 7 May and we started lending on 11 May. We also consulted closely with the British Business Bank throughout this process.

What was the reaction from the British Business Bank when you approached them?

The British Business Bank welcomed our application. Our goal is the same as theirs – to provide financial support to businesses across the UK that are losing revenue, and seeing their cash flow disrupted, as a result of the COVID-19.

Did you need to make any product developments or changes to the business banking offering to cope with BBLS?

Yes, it required a lot of engineering, lending and other expertise. As we’ve said above, we had to launch a new lending platform at scale practically from a standing start. We knew our customers needed this money and we had to get it to them as quickly as we could in compliance with the rules set by the authorities.

The applications for new accounts, once launched, was unprecedented, how did your systems cope with this?

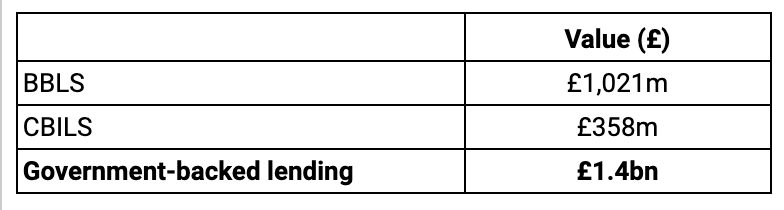

We have a real advantage in that our talented engineers have built our tech platform from scratch. This means that if we need to change something, we can do it quickly, safely and efficiently in-house. Our technology is hugely scalable because our tech team runs a constant simulation at around ten times our current capacity. We’re prepared for a sudden influx of customers and transactions. The proof? Since May we have lent over £1.4 billion to over 40,000 businesses and we intend on carrying on lending until the scheme ends.

If you reflect back on the number of new business accounts and the number of SMEs you have potentially saved from folding, how does it make you feel?

We have never offered cash incentives or metal cards, we are more about honest, simple banking which makes money manageable. We have around £4bn on deposit which indicates that our customers are using Starling as their account.

This was a real shot in the arm for your business banking accounts, which had really only just started getting traction, how will you engage customers to continue using their accounts as they trade out of the pandemic?

We offer the best banking experience in the world, our business account is affordable, forward-thinking and incredibly efficient so I have no doubt that we will retain the majority of new customers we have welcomed during the pandemic.

What are your concerns about potential defaults once the government’s interest and repayment support has finished?

We know there are likely to be defaults. We’re working hard to support customers in a number of ways. This includes our online Coronavirus support hub, advice pieces online and our 24/7 customer service team which are on hand to make sure that our business customers never feel alone.

How much resource does Starling allocate to its business banking function over its consumer side and is it considered the growth area of the business?

We don’t disclose this information but I can confirm that business banking is a growth area for our business and we currently have a 4.4% share of the market.

Is there a revenue model for business banking outside of lending?

Interchange income continues to perform well, having increased over 20% between July and October 2020, despite the increased COVID-19 restrictions put in place around the country in recent months. This is the result of strong primary account growth, as well as increased customer engagement and card spend. The vast majority of our transactions continue to occur domestically with international spend declining after a strong recovery over the summer months.