As businesses shift to a remote workforce throughout the COVID-19 pandemic, organisations are coming to terms with how legacy processes, especially in payments, would benefit from an update to their systems.

Through the release of “The Digital Payments Tipping Point” white paper (E) Brandconnect and WEX Inc highlights how the pandemic has accelerated the digital transformation of B2B payments. This includes statistics that show 62 percent of executives see the need to modernise their technology platforms, given how legacy processes and platforms typically don’t perform as well in a work-from-home environment.

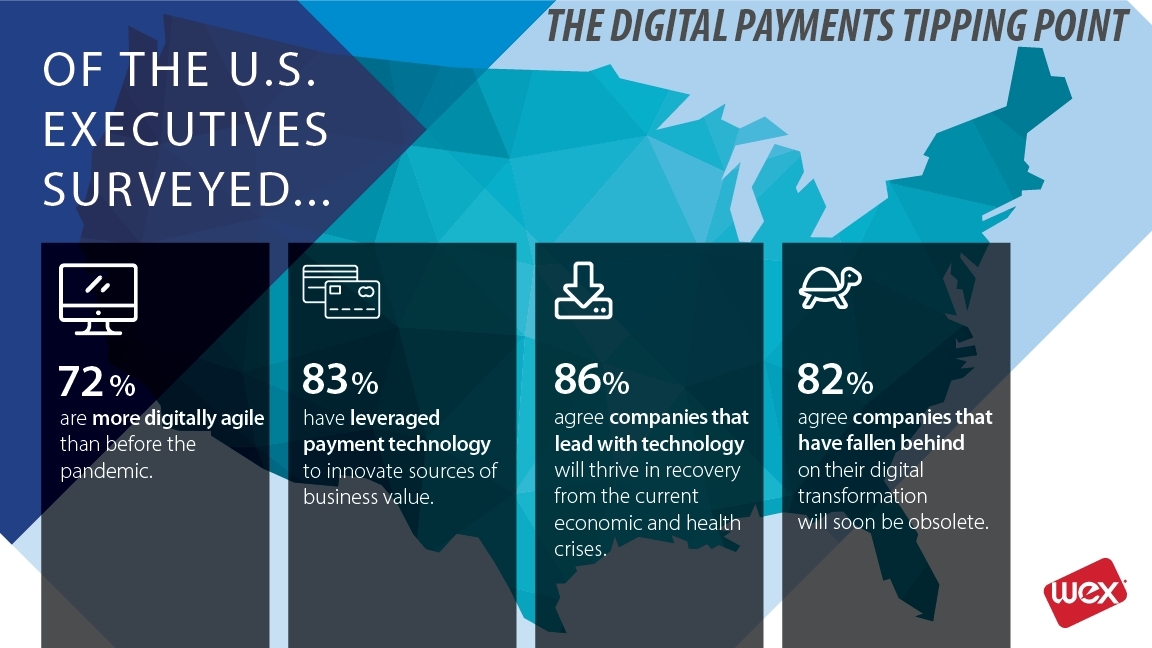

The survey, of US executives in financial services and technology, found that 72 percent of US executives in those sectors are more digitally agile than before the pandemic and 83 percent have leveraged payment technology to innovate new sources of business value.

“COVID-19 transformed the world of work as we know it, and businesses had no choice but to adapt,” says Jay Dearborn, president of WEX Corporate Payments. “In many ways, this was a forced transition but we’ve found that, among our customers and partners, those that are recovering fastest already had a culture of digital transformation instead of relying on legacy processes. Additionally, we are seeing an increased focus on efficiencies and value creation, both from companies making payments and suppliers receiving them.”

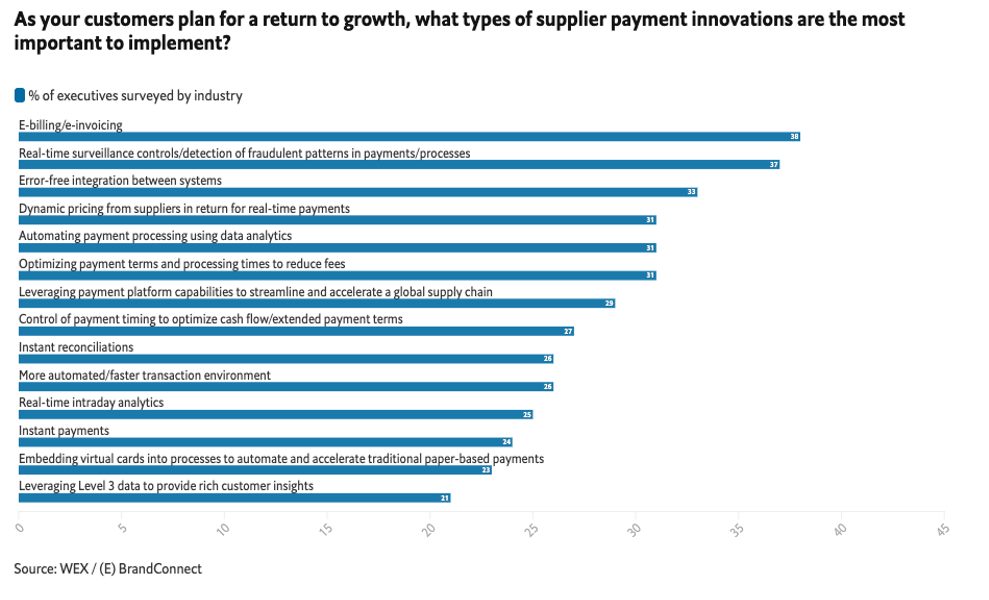

As the economy recovers, 42 percent of those executives say they see the need to modernise their technology platforms, given how legacy processes and platforms typically don’t perform as well in a work-from-home environment. And the race is on: 72 percent of the respondents agree that their company needs to transform its end-customer supplier payments solution quickly in order to outpace its competitors. A deeper look into the findings shows mixed results about the type of supplier payment innovations will be the most important to implement. 38% believe ‘E-billing/e-invoicing is the priority,’ followed by 37% who will focus on ‘Real-time surveillance controls/detection of fraudulent patterns in payments/processes.’

When it comes to creating customer value through payments, 83 percent of the respondents agreed that payments innovations could deliver new business efficiencies and sources of revenue in the post-pandemic economy. Priority areas for payments innovation were identified as e-invoicing/e-billing and cutting costs by optimizing payment terms and timing.

Overall the research highlights both the opportunity and challenges in the payments space, painting a stark reality that companies that don’t adapt may not survive. 81 percent of respondents agree that “companies that continue to lag behind on internal technological infrastructure changes will be left behind” and 82 percent agree that “companies that have fallen behind on their digital transformation will soon be obsolete.”