Banking juggernauts have often been on the back foot in terms of innovation. They wait and see what is successful within smaller companies, then roll out an already successful scheme to their large customer base. With the introduction of challenger banks though, this passive attitude may not work anymore. Experimentation must be done in order to stay relevant and not lose its customer base to new digital companies.

Challenging the challengers is a necessity for incumbent survival. Alex Sion, Managing Director and Co-Head, Global Consumer Bank, D10X, at Citi Ventures and Ron J. Williams, Head of Program Strategy, Global Consumer Bank, D10X, Citi Ventures, discuss how banks must achieve this. Prior to Citi, Williams ran proofLabs, a venture development practice. He has founded, invested in, and advised tech startups for over 12 years and was named one of the 100 most creative people in business by Fast Company for his work as a Sharing Economy pioneer whilst Sion was the General Manager of Mobile for JP Morgan Chase, responsible for Chase Mobile Banking and mobile channel governance for the Consumer and Community Banking Group.

Between the two, they have a wealth of experience in the financial sector and advise incumbents on how to stay relevant:

The pandemic accelerated the use of contactless, digital financial services and e-commerce: 80% of Americans report they can manage their finances without entering a bank branch, and 73% view fintech as the “new normal.”

Consumers, small and mid-sized businesses (SMBs), and even the US government are establishing new habits and preferences for accessing and moving money, showing banking’s future will be tied to the growing and evolving fintech ecosystem. New challengers—including neobanks, non-bank fintechs, and large tech companies—are creating new models of customer engagement, monetisation, product development, risk, and operations.

For incumbent banks, these challengers present both unfamiliar competitive threats and potential new models to follow for long-term growth and success.

New Challengers and Threats

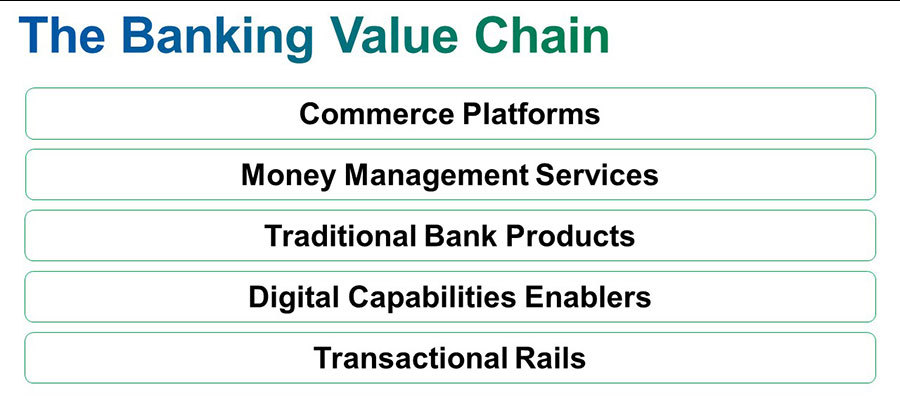

When assessing the competitive landscape, traditional banks usually benchmark their products, organisations, and performance against their peers. However, new threats to incumbents have emerged as API-based digital infrastructures, open banking regulations, and shifting consumer sentiment have given digital challengers and traditional partners (i.e., payment networks) the ability to directly engage with consumers.

These entities target profitable parts of the banking value chain—some closer to the customer, some to the core banking technology—and tend to start by addressing a single need (i.e., peer-to-peer payments). After building devoted user bases they then bundle additional products and services, launching differentiated value propositions and evolving to meet the rapidly changing needs of digital consumers through an array of financial products. Importantly, many of these challengers use APIs to access banking infrastructure without having to carry the full cost of managing the infrastructure—a cost often passed on to traditional banks.

Compared to traditional banks, the challengers are seeing staggering earnings growth. By the end of Q1 2021 one large fintech had achieved 266% quarterly YoY growth, while as of May 2021 another popular challenger’s market capitalisation was nearly double that of some traditional banks—expanding the challenger’s options and the M&A paths open to them for further growth.

Challenger Growth Strategies

Four approaches distinguish new challenger growth strategies from those of traditional banks:

- Solving for the Customer: Challengers that sit “above” incumbents on the value chain are creating products and experiences that are closer to customer end-goals. For example, “buy now pay later” companies are embedding the core “job” of a credit card—helping people make purchases without risking their cash cushion—directly into the shopping experience.

- Solving for Enablement: Challengers that sit “below” incumbents are leveraging partnerships and API strategies to open their infrastructures and make themselves into platforms for challengers higher up the chain. These companies enable the rapid growth of the fintech ecosystem and bring the customer journey together.

- Monetising for Growth: Challengers are exploring nontraditional business models that prioritise sticky growth and customer habituation over near-term revenue. These models, including platform fees and subscriptions, are based on value propositions that feature simplicity, access, or automation on top of a commoditised product or service.

- Operating for Growth: New challengers leverage capabilities including dedicated innovation teams, non-core spinouts, data-driven customer alignment, and ecosystem plays to enable “always-on” growth exploration beyond their core businesses. The resulting culture of experimentation is a crucial enabler of the first three approaches.

Challenging the Challengers

With more challengers expected, incumbents seeking growth may need to move away from the approach of watching the market before innovating and instead begin experimenting quickly with a wider range of customer experiences. Incumbents must find ways to better understand how challenger models work, including by increasing investment in their “playbooks.”

These may include:

- Customer Segmentation: Traditional banks mostly know their customers through “account opening” profiles. By contrast, challengers have created continuously evolving and expanding customer profiles through alternative data, digital marketing, and cloud-based AI/ML technology. These profiles can be used to develop sticky customer relationships, expand addressable target market segments, and drive cross-sell on the basis of behaviour.

- Data Capabilities: Challengers are using customer habituation to rapidly expand into adjacent projects and value propositions. This growth method emphasises nontraditional, nuanced, and long-term performance metrics such as frequency, recency, the amount of customer data, and the projected lifetime value of customers.

- Product Design: Traditional banks have focused on driving growth in core products through financial incentives. Many challengers solve “jobs” adjacent to traditional banking products, such as P2P payments, “early wage access,” financial calculators, automated savings, and investment to support good behavior. Solving these jobs can lead to from SMBs alone.

- Monetisation Models: Incumbent banks often invest in solutions that close gaps, drive account-opening efficiencies, or address predictable business cases. To meet challenger threats, incumbent product teams should instead think like challengers and strive to solve “root-cause” customer problems. They should use distinct growth investments to explore new value-added partnerships and pricing models.

- Fintech Partnerships: Challengers are poised to grow more ubiquitous in the digital banking ecosystem, and incumbents need to find new ways to develop and distribute products and services through them. However, incumbents must also understand the new rules fintechs are writing, the potential risks, and the lessons to be learned. Every partner is a potential competitor, and every partnership is a learning opportunity.

Embracing Change

The future of consumer banking is uncertain—no one knows exactly who the winners will be, what their business models will look like, or how players will compete. With 99% of tomorrow’s fintech market untapped, competitors will come from every corner of the financial ecosystem.

As a result, incumbents should begin now to experiment with challenger models and new avenues for long-term growth. Banks can adopt a portfolio-based approach to the future, investing in both areas of predictable growth and areas of high volatility and uncertainty. By understanding challenger models and applying their thinking to businesses with world-class assets, traditional banks can make great strides in challenging the challengers—and ultimately win.