Earnings on demand apps offer instant access to earned wages. A useful service employees should pay for? Or a loyalty perk employers should provide free?

One thing about lockdown is guaranteed. People who earn by the hour, yet are paid by the month, are going to feel the pinch as hospitality workers join shop staff in starting to get back to work.

The Fintech industry has been offering a solution to access wages earlier than pay day for the past couple of years. However, it is arguably only at this crucial moment, of restarting the economy, that these apps are gaining more public attention. In fact, the niche is so new in the UK that even those offering the technology use different terms.

Whether it is wage streaming, flexible pay or earnings on demand, the principle is the same. A fintech operator’s platform connects to an employer’s pay and HR software to show an employee, via an app, how many shifts they have worked and, hence, how much they have earned so far that month.

The decision is then up to the employee whether to leave the money until pay day at the end of the month or take out a proportion of their wages in advance. Normally, this is limited 40% or 50% of the total wage earned so far.

For many workers it will be a lifeline to put new tyres on a car or buy birthday presents ahead of pay day. However, it does come with an obvious catch. Although the fintech providers will rightly describe themselves as a much-needed alternative to credit card borrowing or pay day loans, there is a fee involved.

An ATM in your mobile

Tom Pickersgill

The newest flexible pay app to launch is Orka Pay from recruitment marketplace, Broadstone. It already offers advance wages for those working through its business but is now rolling out that functionality for companies it sends employees to, such as leading FM businesses. The fee, picked up by the worker, though, is 4.5% of wages drawn down before pay day.

Tom Pickersgill, Co-founder and CEO of Orka Technology Group, believes the new “instant pay” service will be a welcome boon to thousands of workers who want the reassurance of what he likens to a mobile cash machine.

“There are thousands of workers out there who need a service like this to put fuel in their car or pay an unexpected bill,” he says.

“The pay day loans companies are still out there charging exorbitant interest rates, so we’re here to save people getting into an ever-increasing cycle of debt through loans. We also save them from the high fees and interest rates of borrowing on credit cards or using an overdraft facility.”

More flexible workers

Pickersgill points out that earnings on demand apps allow employers to offer a benefit that employees find very useful. At the same time, access to wages before pay day also makes employees more loyal. It can encourage staff to take on extra shifts, when needed, because they know their earnings can be drawn down within an hour or two of having clocked off.

Its experience is that around 40% of those eligible to use the app will do so and the average worker will take out around £70 in advance wages 1.5 times per month. Such widespread use begs a question. Is it right that employers get more engaged workers and yet employees are charged to access a proportion of money they have already earned?

“It’s there as a benefit for the worker, they don’t have to use it,” says Pickersgill. “It’s certainly not something any employee should be allowed to overuse but it does give that reassurance they can pay a bill before pay day without going overdrawn or borrowing at exorbitant rates.”

Employer help

Peter Briffett

At Wagestream, there is a slightly different strategy. It charges employers, depending on their size, between £2.75 and £1.25 per month to have an employee on its app. It then charges a flat fee of £1.75 per ‘stream’ – its term for each time the app is used to download earned wages.

However, it is not always the employee who picks up this cost, as Peter Briffett, the service’s CEO and co-founder points out.

“Five of our bigger customers pay for the first two uses of the app in any month, and that’s something we encourage all the employers we work with to consider,” he says.

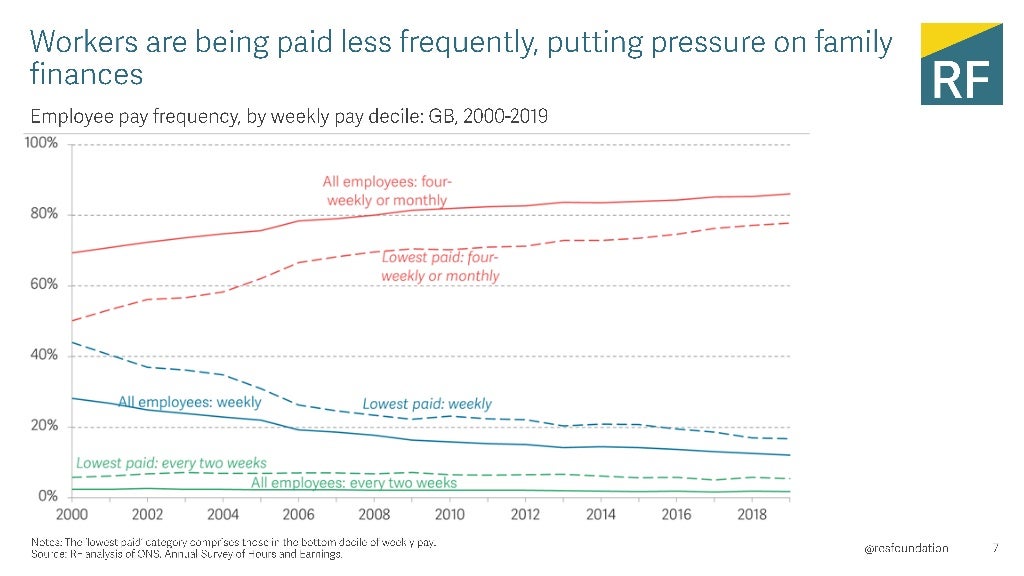

“It’s hard to argue against people being given free access to money they’re already earned, even though £1.75 is effectively what they could pay at some ATMs anyway. The nub of the issue is that we’ve moved from weekly pay to monthly pay becoming normal. In USA just about everyone gets paid on a fortnightly basis. It means UK employees are far more exposed to unexpected bills.”

Graph courtesy Resolution Foundation: https://www.resolutionfoundation.org/

Instant earnings card

Peter Ingram

At Hastee, the notion of instant wages is being taken a step further and applied to a card, launched last month. It cuts out the task of a worker having to use the app to download money to a bank account before it can be spent. Instead the Hastee Card can be used like a pre-paid debit card, limited to that employee’s available balance.

The Hastee Pay service allows any user to take out £100 for free each month. Thereafter, withdrawals come with a 2.5% transaction fee. Hastee’s CTO, Peter Ingram, points out several employers choose to cover a further two transaction fees per month per employee. Although the company falls into the modern fintech sector, he believes its core promise lies in providing a bridge back to the old days of workers being paid weekly.

“We’re effectively invoice factoring for humans,” he says.

“The problem is technology has given us a whole host of new ways of paying for things, such as contactless cards, mobile wallets and PayPal, but at the same time people have gone from being paid weekly to monthly. They’re effectively giving a month’s worth of labour as a credit to their employer.”

Fintech executives may be excited by the advances they can offer cash-strapped workers and employers are also keen to keep employees more flexible and loyal. Wagestream’s Peter Briffett claims the company’s research has shown employee churn rates are reduced by 16% when businesses embrace earnings on demand.

Charles Cotton

However, at the Chartered Institute of Personnel and Development (CIPD) there is a call for caution if any tech company thinks this is a panacea. Its Senior Policy Advisor for Pay and Reward, Charles Cotton, has a balanced view. While he believes apps that provide access to earned wages are useful, they should be seen as a starting point rather than the whole picture.

“These apps are not a silver bullet, employers need to take a wider approach,” he says.

“The obvious point is that businesses could think about whether they’re paying people enough, if they are in financial trouble. That may not be possible, but paying people on a more regular basis is an obvious step forwards. So too is providing insurance against, say, sickness and also offering a hardship fund facility through which employees can occasionally borrow money to meet an unexpected bill.

“Investing in financial education is also advisable because our research has shown one in four employees are so worried about money it affects their ability to do their job.”

So, apps that allow employees to draw down money they have already earned are undoubtedly very useful. They become even more appealing to employees when employers cover all or some of the cost of occasional use.

The advice from HR experts, though, is for employers not to rely on them exclusively but to offer a pay and wellness package. This can ensure earnings on demand services are a safety net, not a regularly-used mobile ATM leaving workers with a hole in their wages each month.