Deteriorating macroeconomic conditions and rising inflation pressures leave little room for payments failures, costly errors and operational delays.

Dalbir Sahota, senior director of product management – Bankers Almanac Payments & FC KYC at LexisNexis® Risk Solutions, has more than 15 years’ experience working in investment banking operations transformation covering the domains of client data, foreign exchange services, derivatives middle office and KYC/CLM.

Here Sohata provides valuable insights into the importance of efficient and secure payment processing for businesses operating in the global economy.

The rise in ecommerce and cashless transactions continue to fuel growth in revenue from global payments, which is expected to reach $2.3trillion by 2026. That’s up 8.3 per cent from a reported $1.5trillion in 2021.

The rise in ecommerce and cashless transactions continue to fuel growth in revenue from global payments, which is expected to reach $2.3trillion by 2026. That’s up 8.3 per cent from a reported $1.5trillion in 2021.

Failed payments are the dark cloud in an otherwise silver lining of revenue growth. With an estimated cost to the global economy of $118.5billion per year, the impact of broken or failed payments is too large to ignore.

No organisation is immune. Failed payments impact businesses of all sizes, across all geographies, and across industries – from banking and financial services to telecommunications, energy and e-commerce.

According to the True Impact of Failed Payments, a recent study by LexisNexis® Risk Solutions, 49 per cent of organisations surveyed indicated that broken or failed payments have a severe impact on the cost to the business. More than 70 per cent said they were not satisfied with their payment failure rate. It is no wonder that reducing failed payments and improving straight through processing (STP) rates are ongoing priorities and among the top payments trends this year.

Direct costs of failed payments impact your business

A failed payment is one that is rejected by a beneficiary or intermediary bank within the payment flow. Payments can fail or be delayed for a number of reasons.

Missing or inaccurate bank beneficiary name and address details is the most common cause for payment delays or failures, followed by issues with non-IBAN account numbers and bank name/SWIFT BICs. Improper formatting, poor reference data, the validation tools used, and how payments data is accessed can also contribute to rising payment failure rates.

Many organisations still rely on manual checks – which are time consuming and prone to error – before sending a payment. According to the LexisNexis® Risk Solutions study, nearly 75 per cent of organisations check bank beneficiary name and address details manually; and 51 per cent check non-IBAN account numbers manually.

The average global fee for rejected or repaired payments is $12, with larger companies typically facing higher fees. This is likely due to their use of more expensive banks or more advanced (and costly) solutions.

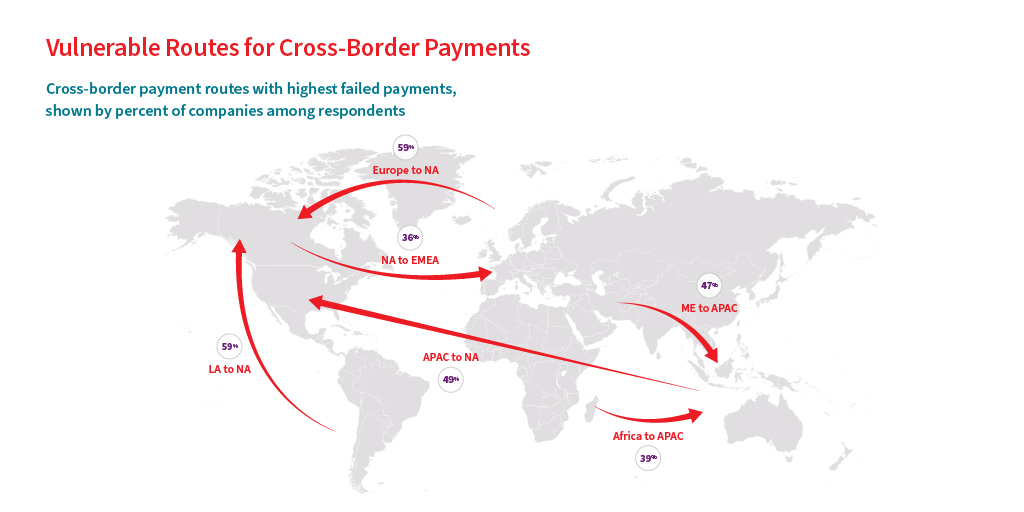

Geography also plays a role in payment failure rates, with some global payment routes more vulnerable than others. Cross-border payments from Europe to North America and from Latin America to North America have the highest rate of failure at nearly 60 per cent for each route.

Indirect costs take their toll

In addition to direct costs, the indirect costs from failed payments reach deep and broad into an organisation – increasing staff workload, challenging safe payment verification and fraud prevention, and potentially compromising the reputation of an organisation. There is also the impact on customer and supplier relationships to consider.

Customers and suppliers have come to expect fast, frictionless payments. The ability to deliver a seamless experience can serve as a strong differentiator and a way to effectively compete in a crowded market. But, getting the customer experience wrong can be detrimental to business. About 50 per cent of organisations report losing customers due to failed or delayed payments and 47 per cent say that failed payments have a severe impact on customer retention.

Straight-through processing makes smart business sense

Straight-through processing (STP) is akin to an automated highway. It helps speed payments so companies can deliver a seamless end-to-end customer journey with as little friction as possible.

In fact, organisations identified speed of processing and reducing manual intervention as two of the top three essential elements for efficient payments processing. These were surpassed only by the accuracy of payment details, which 40 per cent of organisations ranked as the number one essential element for efficient processing.

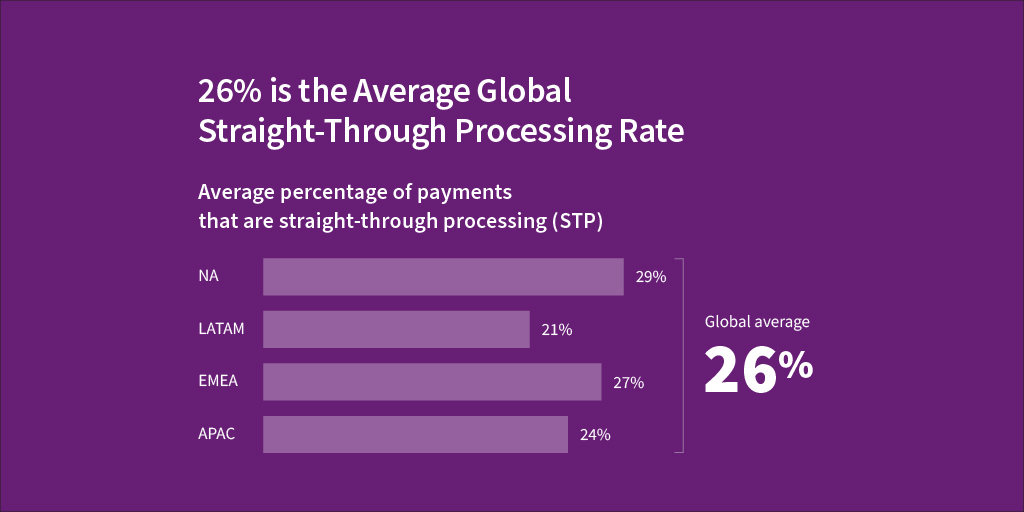

With a global average of only 26 per cent for straight-through processing of payments, finding the optimal balance between accuracy and speed is clearly challenging. Although the average STP rate varies somewhat by region, industry, and size of organisation, the low overall STP rates reflect untapped potential to achieve greater end-to-end efficiencies.

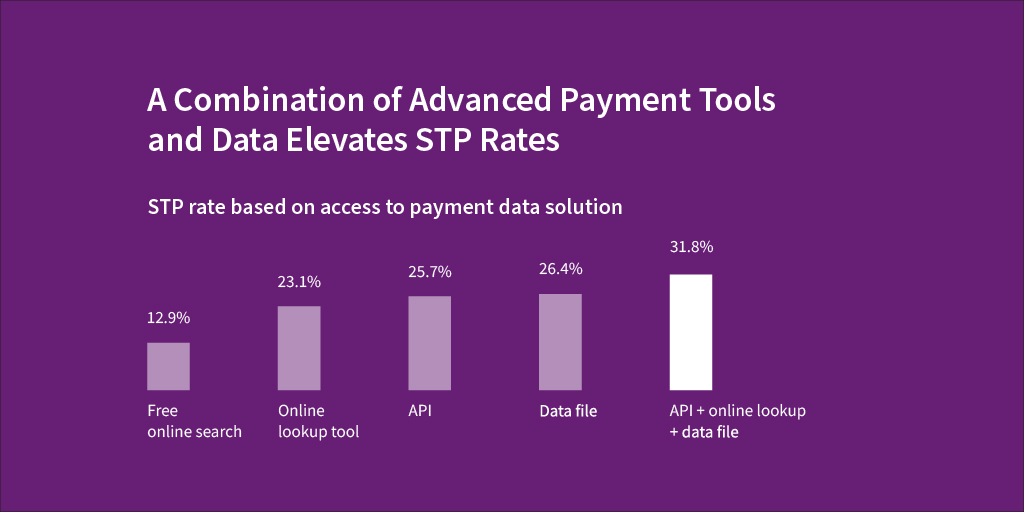

Raising STP rates can best be accomplished with a combination of accurate, accessible payments data and advanced payment tools. For example, the LexisNexis® Risk Solutions study shows that combining APIs, online lookup, and data files can boost STP rates to 31.8 per cent compared with 23.1 per cent for an online look up tool alone or 25.7 per cent for APIs.

Advanced payment tools safeguard against fraud

Authorised push payment (APP) fraud – where a victim is tricked into making a real-time payment to a fraudster – is a growing concern worldwide. These scams account for 75 per cent of all digital banking fraud based on dollar value, according to a report from Outseer. Losses to APP fraud are predicted to double to $5.25billion by 2026.

By incorporating advanced API payments technologies, including safe payment verification tools that instantly verify customer-entered information, organisations can prevent APP fraud and ensure the payment is going to the true intended end recipient. These solutions work in the background, offering a frictionless process that does not weigh down operations with time-consuming manual lookup, added costs, and unnecessary delays that slow payments and test customer patience.

Payments efficiency is built on accuracy, speed and security. Organisations that leverage API technology and the most up-to-date global payments data will be better positioned to deliver a superior customer experience, raise straight-through processing rates and meet the operational challenges of a rapidly changing market.

Supercharge your payments processes today.