For several years now I’ve been talking about Blockchain’s capability to create global public infrastructure in a new way – digital of course and much faster than we’re used to when we talk about infrastructure. In months or years rather than decades. Orders of magnitude cheaper.

My words seemed to have fallen entirely on deaf ears – perhaps because this was too big an imaginative leap. Especially for those yet to grasp Blockchain’s capabilities, and that this is its raison d’etre.

Now I’m not so sure. It was a little over six years ago that I was invited and scheduled to go to China as a delegate to a major conference on Financial Innovation. I even got my visa sorted ready:

As it turned out for various reasons I was unable to go, but in the interim, we had various encounters and pre-meetings in Leeds, Sheffield and thereafter the Chinese were very active indeed in various APPGs, sponsoring a variety of them, providing ample funding for their secretariats.

China’s Global Public Infrastructure

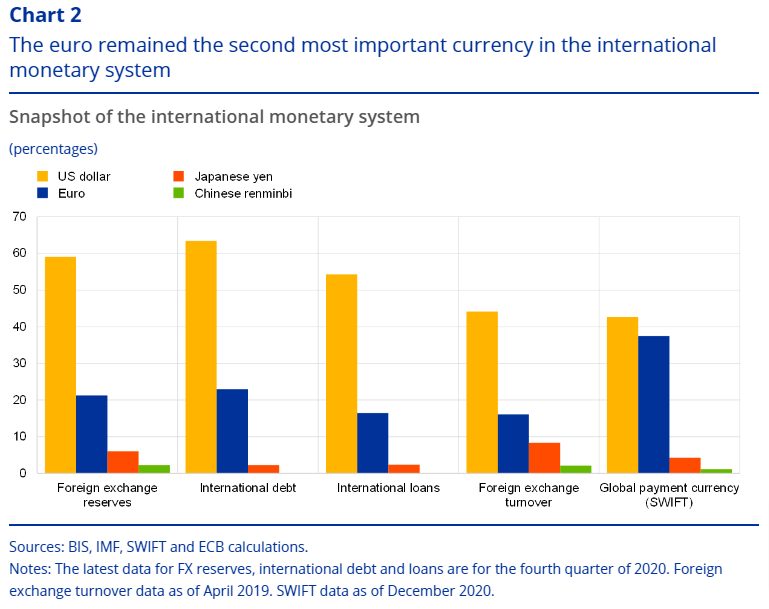

As they move forwards with public trials of their CBDC it’s now becoming increasingly obvious that China has leapfrogged the west in doing just that: creating global public infrastructure to facilitate global trade with low-cost, low-friction payment facilities fully integrated based on its new digital currency the e-Yuan.

In the last couple of weeks, it has become increasingly clear that this has been dawning on strategists in Washington and Brussels via a trickle of underreported announcements from each.

Carefully Measured Public Reactions

Not long after the Fed quietly abandoned its ‘there’s nothing in it for us – we have the dollar’ stance in a carefully worded speech delivered on 24th May at Consensus 2021, the Fed’s Lael Brainard admitted that:

“issuance of a CBDC in one jurisdiction can have significant effects across the globe, so it’s very important for us to follow many central banks’ progress on CBDCs.”

“…some foreign countries have chosen to develop and, in some cases, deploy their own CBDC. Although each country will decide whether to issue a CBDC based on its unique domestic conditions, the issuance of a CBDC in one jurisdiction, along with its prominent use in cross-border payments, could have significant effects across the globe. Given the potential for CBDCs to gain prominence in cross-border payments and the reserve currency role of the dollar, it is vital for the United States to be at the table in the development of cross-border standards.

In response to a question from the moderator, Brainard admitted they are now “paying attention to how other countries, like China, aredeveloping their own CBDCs.”

On stablecoins she also said:

“If widely adopted, stablecoins could serve as the basis of an alternative payments system oriented around new private forms of money. Given the network externalities associated with achieving scale in payments, there is a risk that the widespread use of private monies for consumer payments could fragment parts of the U.S. payment system in ways that impose burdens and raise costs for households and businesses. A predominance of private monies may introduce consumer protection and financial stability risks because of their potential volatility and the risk of run-like behaviour.”

European Central Bank Report

Eyeing the potential for the digital Euro (and the threats of not creating one the ECB is admitted its concerns about a situation developing “in which domestic and cross-border payments are dominated by non-domestic providers” in its report dated 2nd June, adding “attention should be paid to the risks to stability that might arise if a central bank does not offer a digital currency” as well as assessing the upside.

The ‘European Digital Identity Wallet’

In a highly coincidental (or otherwise coordinated) move, the EU’s Executive Commission unveiled their plans for a digital ID wallet as part of their post-pandemic recovery strategy, which involves accelerating the shift to online. With the dominant online platforms required to accept the wallet. Aligning with the commission’s goal of reigning in big tech companies and their control of personal data.

China’s Offering – US Reaction

While China’s offering will not just be internal but also to the world it is not so much a frontal assault on the dominance of the dollar (and all that entails) as building on the successes of WeChat and Alibaba – combining them with a state-backed digital currency, with all that it entails:

– Easily accessible / Available everywhere

– Friction and (largely) cost-free transactions that can seamlessly cross borders

Most likely also adding easily accessible trade credit, powered by AI.

Think Next-Generation, Integrated…

To get a feel for this, think of a more accessible, next-generation, Amazon AWS at a fraction of the costs and with next-generation payment integrated. Plus likely Paypal-style trade-credit.

Whether the US (and EU) will seek to raise barriers, which seems a possibility especially in the case of the US, remains to be seen.

But even if this were the case much of the rest of the world could certainly benefit and is likely to welcome this with open arms. Whatever other strings may or may not be attached by China some are intrinsic – not least reliance on China and its future policies.

A New Cold War – or a Not-so- Extraordinary Challenge to Capitalism on its own terms?

In the US there has already been loose talk of escalation and a new cold war centred on China. However, if China is playing the west at its own game – and it is – then the appropriate (and safe) response from a capitalist / democratic viewpoint is surely to compete?

So is it not increasingly clear that seeing the possibilities in new Blockchain and AI, China has spent the last six years so well as to now be in a position to leapfrog the west – if it has not done so already? And that this is now dawning (because it can no longer be denied) in the capitals and central banks of the world? With governments ill-equipped to understand, let alone address the deep structural issues and challenges that ensue.

We knew the possibilities existed. Indeed some of us have been pointing to them for years now, while politicians waited for the markets to take care of it. That does not seem to have worked so well in this case.

What is certain is that navigating what is already a complex and fast-moving global paradigm shift will be a major challenge for all involved. To help lead and influence the outcome in favour of transparency and diversity will require a much better response than anything in sight. We will need a strategy based on clear thinking going forward – and on a clear understanding of both the frontier tech and its possibilities and developments globally.

This is why I’m convening a series of global strategy workshops during June and July with invited guests from around the world – for both policymakers and those who understand the tech and its implications – and can suggest answers for the most pressing questions. To shed some light and help strategy formation.