In a financial system besieged by the digital revolution, financial and insurance companies find themselves faced with opportunities and challenges imposed by new technology and with growing competition coming from both inside and outside their sector. For these players it is necessary to commence, or in some cases continue with more resolve, what we call the Open Finance Journey, a path of Open Innovation in all areas of the financial and insurance world.

In its “Open Finance in Europe” report, the Fintech & Insurtech Observatory of Politecnico di Milano analysed 256 financial services offered by 55 players that do not come from the world of finance – automotive, retail, utilities and tech companies – but who, simultaneously, add competitive pressure and offer new cooperation opportunities for the more consolidated players.

Filippo Renga, Alessandro Faes and Dana Bonaldi, Fintech & Insurtech Observatory, explain the key elements of the report.

Financial services from external players

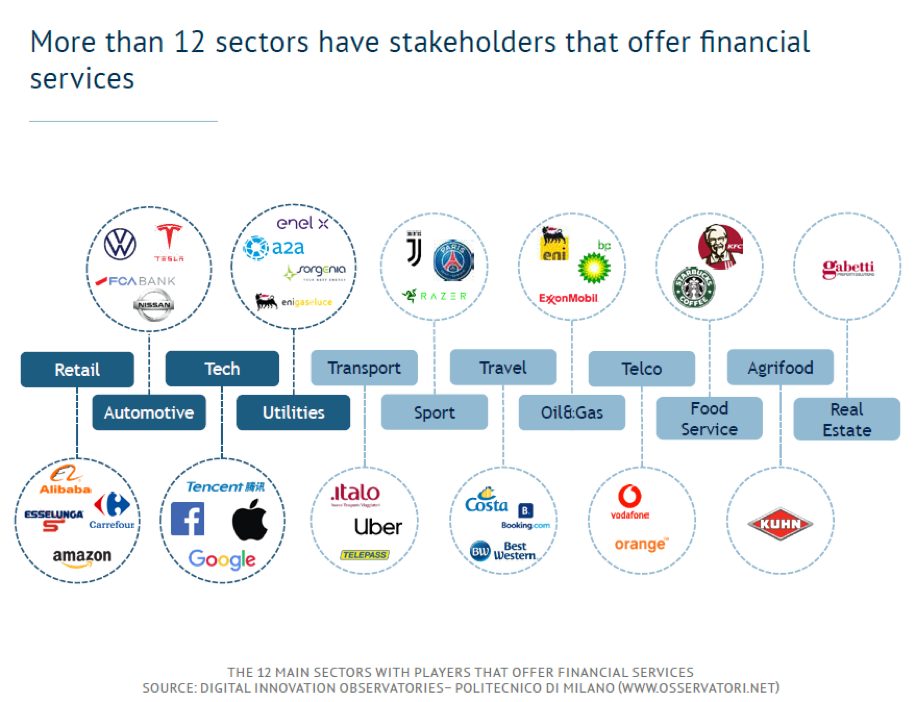

The Observatory Research reveals players from 12 different sectors that offer financial services, created in-house or in partnership with other financial players.

The examples range from the best-known cases such as Apple Pay for payments, or Amazon Lending for loans, to less well known services such as Fan Tokens based on Blockchain, offered by the football teams Juventus and PSG, travel insurance offered by players such as Booking and Costa Cruises, or payment cards offered by fuel retailers such as ENI.

Our analysis concentrated on the four most active sectors, with financial service proposals based on assets that are significant for the future of Finance (user base, customer engagement, financial resources, etc.). The four sectors are Tech, Automotive, Utilities and Retail, which also includes eCommerce players. In these four sectors we identified 55 players who offer a total of 256 financial or insurance services in Europe (intended as EU-28).

The most commonly offered services are insurance services (41% of the total) and they include, for example, life cover, home insurance, credit insurance or extended guarantees. Next come loans and financing services (31%), such as consumer loans, mortgages and leasing, and payment and transfer services (18%), such as credit cards or Mobile Payment. Savings and deposit services are less common (9%). These include current accounts or savings accounts, and finally investment services (only 1%), such as trading platforms or investment funds.

In the Retail and Utilities sectors, offerings of insurance services are most common (43% and 66% of the total, respectively), and they range from cover related to the product sold (for example Amazon Protect) or gas or electricity provision, to wider covers (such as life, home or animals).

Offerings in the Automotive sector are dominated by insurance and financing services (36% and 37% respectively), both associated with the vehicle purchased by consumers, and in some cases offered to the general public through a real bank. 100% of the players considered offer both types of service, showing consolidated activity in this sector.

Among the players in the Tech sector, the most common services are loans and financing (58%), usually for the purchase of technology products, but some go further, to offer more complete financing services (for example, an IT supplier in the UK who offers Invoice Financing services to companies).

The main business strategies

The report has also identified four main strategies for offering financial services among these players. On the one hand, 45% are “traditional”, offering only financial services to their current clients and linked with their core business, such as financing for a car purchase offered by the Automotive sector.

On the other hand, 35% of players offer financial services that are not strictly related to their own core business and are aimed at new clients (“Open Finance Oriented”). These players place themselves in direct competition with financial institutions, while also offering more cooperation potential. 79% of these cases have even founded a bank or insurance company.

In between these two groups, 18% offer new services that are not linked to their core business, but are aimed at existing customers, to in this way explore the possibilities offered by the Finance sector (“Explorer”). There is just one case of a company that offers a service related to their core business, but used to reach new clients, operating like a “Trojan Horse”.

There are more than 15 players who offer part of their range of financial services only in countries outside of the EU, but who could extend to our continent relatively easily, given their wide customer base and consolidated channels, creating potential competitive pressure on our financial system. The main Big Techs include Apple, for example, which started to offer credit card services in the USA this year with Apple Card, or Facebook, which currently does not offer any financial services in Europe, but offers mobile payment services in the USA.

From Asia we could see the arrival of Alibaba and Tencent, which currently only offer their payment services in Europe (AliPay and WeChat Pay respectively), but in Asia offer clients a wide ecosystem of financial services, including investments, and Samsung which offers more advanced payment services in the USA and Asia than it does in Europe (for example, P2P transfer services).