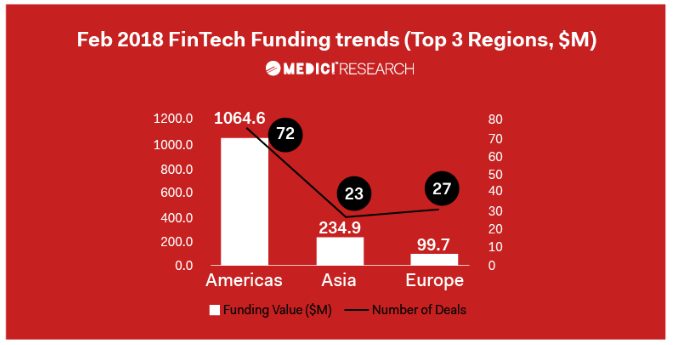

Europe remains one of the top regions for fintech investment, coming only third to (the much larger regions) of the Americas and Asia.

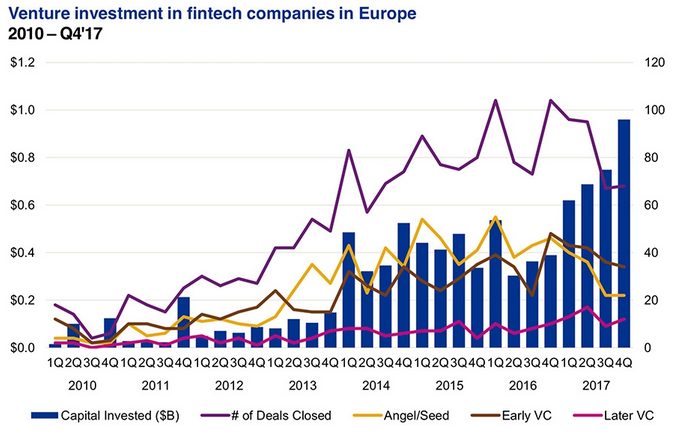

What is interesting is that, although total investment activity is down from the highs we saw from 2014 to 2016, VC investment specifically has actually grown considerably during 2017.

Partner at Index Ventures (a VC firm which was founded in Geneva and headquartered in London), Jan Hammer, previously said that there’s an upward trend of US funds looking to come and invest in Europe because European companies seem to have the ability to scale globally much quicker than anywhere else.

“Clearly there are a number of sectors and themes where Europe has the cutting edge — I would call it thematic expertise. Go back to fintech, this is why I spent the vast majority of my time on fintech, it’s because the ecosystem [in Europe] is very fertile.”

Tom Wilson, investment manager at Seedcamp (who raised a £41 million fund – around $57 million – in late 2017 for startup investment across Europe) shares this optimism for the European fintech market.

“Personally, I’m very bullish on Europe. I think it’s a great time for founders to start businesses in Europe because there’s a strong supply of talent and the funding environment is buoyant with a number of large established VC funds complemented by an increasing amount of new funds.”

International VC investor Oleg Boyko, chairman of Finstar Financial Group, calls the fintech industry “the largest Blue Ocean opportunity” in the world. “There are no other commercial sectors that have so little competition”, Boyko continued.

Regional change

Within Europe itself, there’s a small shift as well, with investors realizing there are other opportunities outside of the normal fintech hubs of London, Germany and France. In recent times there’s been an increased focus on CEE countries (Central and Eastern Europe). The CEE fintech market is worth an estimated €2.2 billion ($2.6 billion).

Oleg Boyko of Finstar sees this growth in emerging markets such as the CEE region, as a great opportunity for fintech startups. “The rapid growth in consumer demand across the emerging markets offers exciting opportunities for fintech-enabled disruptive lending technologies. With our market-leading expertise, Finstar can capitalize on these emerging trends.”

The company, who have $2 billion AUM, will increase their portfolio exposure to emerging markets across Europe and other high-growth regions such as Latin America and Asia-pacific with their five-year investment plan that focuses on innovative consumer technologies.

This view is backed by other VC investors. With a $100 million fund, Speedinvest’s founder and CEO, Oliver Holle, said, due to the emergence of technical talent and sophistication in this region, the fund will focus particularly on startup investments in the CEE region.

James Wise, a partner at Balderton Capital, agrees that, with the right talent on board, great companies can be built from anywhere around the world.

“There is talent here and an increasing amount of support for founders. The view that tech companies can only be built in big cities like London and San Francisco is quickly becoming outdated.”

Specific technologies

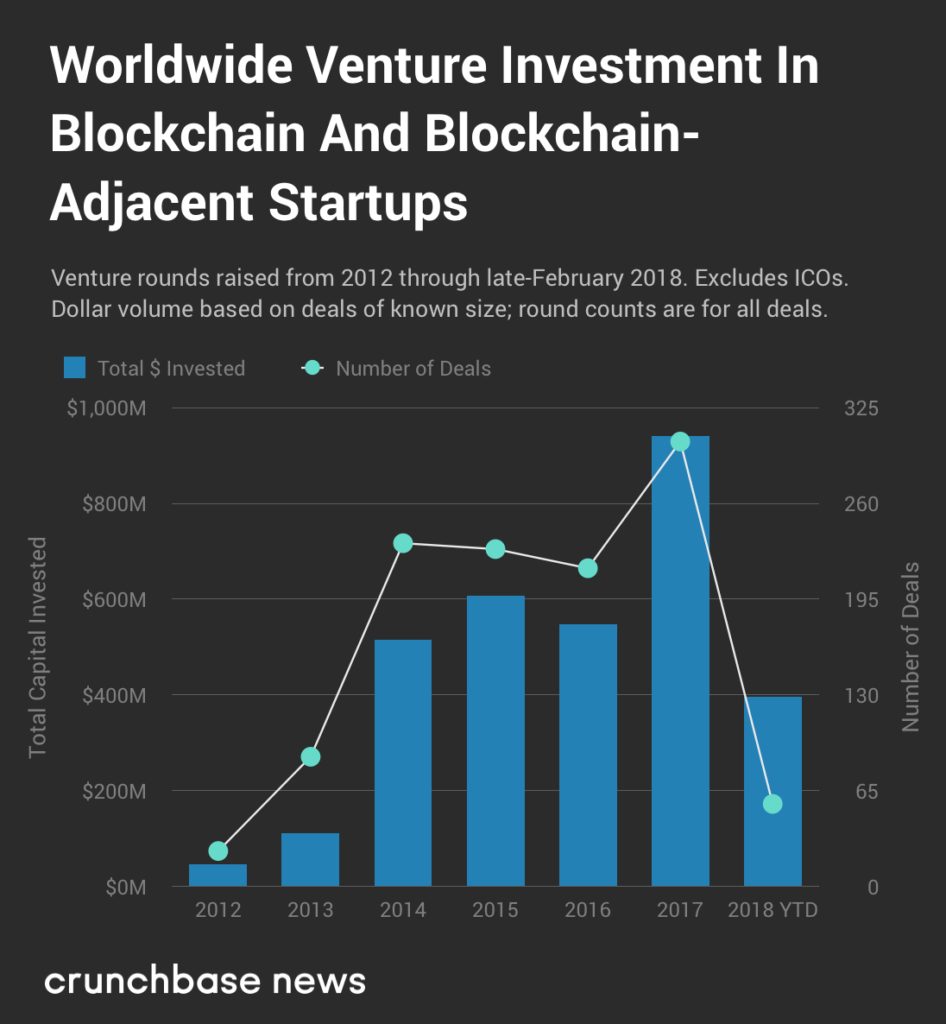

These days it’s hard to talk about fintech trends, without mentioning Blockchain. This is in part due to the huge attention it is attracting through the crypto industry. But Blockchain related investment, outside of the crypto world, is getting a lot of attention as well, mainly because of its potential to revolutionize traditional financial sectors.

Tom Ryan, divisional head at Anthemis, agrees on the revolutionizing potential of Blockchain but say it’s time for more practical applications.

“Our view is that we want to see more actual development and less consortium building and over-capitalization. We want to see more execution, whether that’s in health insurance or for tracking wine portfolios or diamonds. There has been a lot of capital and attention focused on it to date. Now it’s time for more application and execution.”

Insurance is another area of interest. It’s one of the oldest industries on earth and therefore perhaps not so surprising that fintech startups are targeting outdated systems and platforms within the sector.

“Insurance is obviously an exciting investment theme – you’re talking about 300-year-old companies with high margins and low customer satisfaction. It’s no secret that the current models are flawed and that insurance as we know it will change dramatically” continued Ryan.

According to KPMG’s Pulse of Fintech report, VC investment into InsurTech reached a record high of $2.1 billion in 2017. InsurTech consistently showcased in the top 3 most funded fintech segments in the first three months to March 2018.

Cybersecurity in financial services is also a top concern for many leaders within the industry. So much so that 86% of financial services firms across Europe and the UK are planning to increase their cybersecurity budget.

In the three years from 2014 to 2017, the cost of cybercrime to financial institutions went up by more than 40%, from $12.97 million per firm, to $18.28 million (Accenture). At £11.7 million per company, the average across all industries is much lower.

We are therefore likely to see more fintech startups focussing on cybersecurity.

“The new reality for most companies is that they are facing more and more sophisticated criminals who have platforms to share information and buy tools on the dark web”, said Sam Myers, a Principal at Balderton Capital.

He continued, “At the same time, governments are putting more responsibility on companies to protect their customers, making future breaches a lot more expensive than they have been in the past. All-in-all, demand for security products is higher than it’s ever been and there’s a lot of room for new tech companies to play.”

Challenges and the future

Fintech’s exceptional growth over the last few years is also the source for the industry’s biggest challenge.

In an attempt to get a grip on the sector, governments and regulatory bodies tend to enforce excessive regulation, the cost of which can prove too much for fledgling fintech startups to bear.

This is a major inhibitor to innovation.

But even in this area, Europe seems to come out on top, with progressive legislatures, such as the EU’s Second Payment Services Directive (PSD2) that went into enforcement earlier this year, setting the tone for regulators across the globe.

And what of the future? According to Oleg Boyko, the fintech revolution will continue to grow to create a more inclusive financial ecosystem, that’s ultimately more cost effective with a frictionless user experience for customers.

“Big Data, artificial intelligence, complex algorithms, mobile and cloud computing, AdTech – it is all combining to create a revolution in the financial services sector. After this revolution financial services will be available to far more people than currently, in many more markets, be more affordable, be far better tailored to the individual consumer, and be an infinitely better, smoother, more convenient experience for customers.”