Initial Coin Offerings (ICOs, also known as Token Generation Events) have taken the fundraising world by storm. Over $3.5 billion were raised through ICOs last year. It forced legal framework developments, with respect to enabling ICOs, on a global scale. We invite you to examine the most popular global jurisdictions in the ICO universe.

Vast sums of ICOs have been raised in support of new blockchain-based ventures, platforms, services and technologies – often in record times. Notable examples were FileCoin’s $257 million raise, Tezos’ $232 million raise, and Sirin Labs’ $157 million raise – and this was last year. It is of course an open question as to whether these ICOs (or pre-ICO SAFT raises), would still be viewed as fully legal in 2018, or whether they would have raised similar amounts.

Inherently Global

Part of what makes this ICO development so exciting is how inherently global it is. This universality makes intuitive sense since blockchain technology is itself a global, almost borderless, technology. Yet, as global and universal as the blockchain and crypto phenomena are, the ventures which create these new platforms, and especially those which engage in ICO fundraising, are almost always themselves “real life” legal entities (limited liability companies, corporations, nonprofit foundations, and/or some combination of these).

Furthermore, these entities are often formed in diverse countries, states, provinces, and territories, as ICO promoters seek to put themselves in legally advantageous and protected positions. Foremost on everyone’s minds are the legal concerns relating to securities regulation and tax law, although other considerations can, and do, play a role.

Since each jurisdiction is unique and offers its own heady blend of features, opportunities, costs, and “gotchas”, the selection process is not trivial. This article will examine the most popular global jurisdictions in the ICO universe.

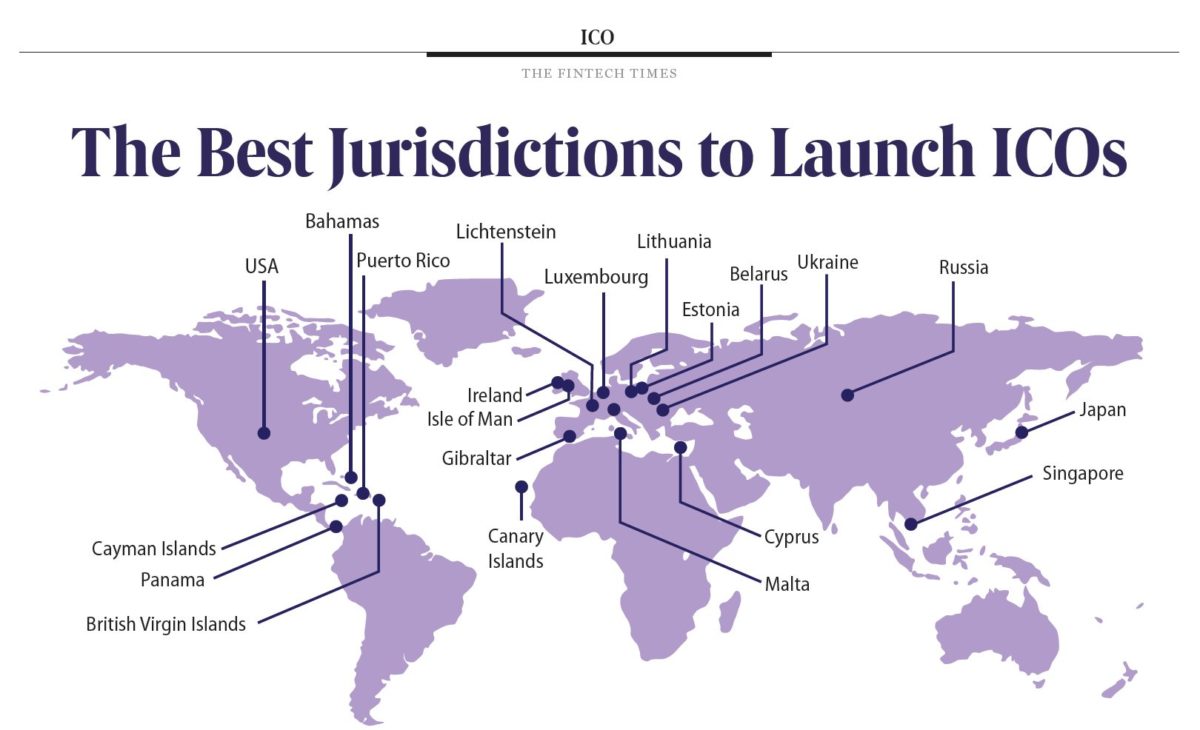

A non-exhaustive list of the most popular jurisdictions in the ICO universe:

- United States (Puerto Rico, Delaware, Wyoming, etc.),

- Gibraltar,

- Malta,

- Singapore,

- Switzerland (Zug, etc.),

- Ukraine,

- Russia,

- Cayman Islands,

- British Virgin Islands,

- Canary Islands,

- Panama,

- Isle of Man,

- Belarus,

- Estonia,

- Lithuania,

- Israel,

- Lichtenstein,

- Luxembourg,

- Cyprus,

- Bahamas,

- Japan,

- Ireland (for intellectual property).

Competition with Each Other

The attentive reader will note that several of these jurisdictions seem to be in competition with each other.

For example, Malta just came out with its new DLT regulatory structure. Gibraltar has new regulations arriving, along with its new exchange dedicated to blockchain assets. FINMA in Switzerland recently release new “guidance” (not regulations) regarding the characterisations of certain ICOs and tokens. One anecdote I recently heard was that an upper-level regulator in one jurisdiction specifically asked an ICO consultant what his country needed to do in order to stay competitive with a certain other nearby jurisdiction.

What is also interesting is the extent to which these jurisdictions are seeking to synchronise with each other. Rather than necessarily engaging in a regulatory “race to the bottom”, in some cases there seems to be coordination and discussion between jurisdictions. To the extent that this lessens the overall regulatory burden being faced by ICOs, the better it will be for the world as a whole.

In the meantime, the Securities and Exchange Commission in the United States seems to be taking a tough line with its statements, but actual enforcement has not necessarily been quiet as harsh. Yet, everyone seems to expect the United States to come out with new regulation soon. One final thought before we wrap this up, pending the first jurisdictional deep dive. It is this – by carefully selecting jurisdictions based upon their unique features, and by mixing and matching as needed/required by the unique circumstances being faced by any particular ICO, it is in some ways possible to create a “virtual jurisdiction”.

For example, an ICO may select the Cayman Islands as its banking jurisdiction, Puerto Rico for taxes, Gibraltar for its exchange, the Isle of Man for its gaming, etc. Obviously, this is a hypothetical example and the reality is far more complex. But, in a sense, each jurisdiction’s particular law is just a pixel making up part of the bigger picture. Of course, everyone cares about this or that SEC, FINMA, Gibraltar or Maltese pronouncement.

Gordon Einstein, Managing Partner at CryptoLaw Partners