Kate Goldfinch (Science Editor)

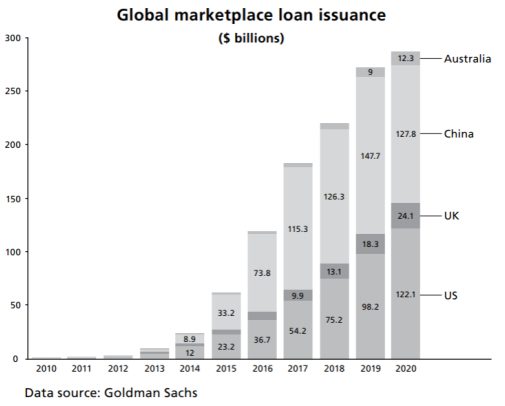

Digital lending has great potential to reach people who have so far not been involved in financial services. The rapidly growing online lending marketplaces (dubbed peer-to-peer, or P2P, lenders) and established financial institutions compete to find out who can provide borrowers with more funding and better terms. According to Autonomous research, by 2020 digital lending will encompass 10% of all loans in the U.S. and Europe at $100 billion in volume.

According to Wikipedia, P2P lending is the method of loaning money to individuals or businesses through online services that match lenders with borrowers. It involves debt financing that enables individuals to borrow and lend money—without the use of an intermediary. Peer-to-Peer lending removes the middleman from the process, allowing cheaper and faster financial services.

The volume of global P2P payments and remittances is eclipsing $1 trillion yearly, with per annum growth rates in P2P lending volumes reaching 50-80% in various markets during the past few years. The appearance of digital technologies, blockchain, and cryptocurrencies such as Bitcoin, has also facilitated consumer and investor adoption to online marketplaces.

Who’s who in digital lending

Today, P2P platforms are among the fastest growing segments in the financial services space. Each platform in this space leverages technology to offer loans directly for the customers – faster and less costly.

Zopa was the first online personal finance P2P lending company, and others in the U.S. and Europe have followed, including LendingClub Corporation (LC), Prosper Marketplace, Upstart, Prodigy Finance, Funding Circle, CircleBack Lending, Peerform, Pave, Daric, Borrowers First, SoFi, Ratesetter, and Auxmoney. Notable local dominant digital lenders include Konfío in Mexico and Kenyabased Kopo Kopo.

Tech giants have also joined the digital lending ecosystem. Since 2012, Amazon has offered small business loans through their lending programme. “Amazon grabbed headlines by giving $1 billion in smallbusiness loans to over 20,000 merchants in the United States, Japan and the U.K. Their near real-time data on sellers’ businesses and access to customer reviews allow Amazon to evaluate customers and manage the risk of lending to small merchants,” Priya Punatar, Industry Engagement, Global Advisory Solutions at Accion, says. “WeChat also made waves when it entered the game in 2015. As China’s largest social network, it’s been able to deploy more than $14.7 billion in funds in just two short years. Like Amazon, WeChat benefits from access to data and the ability to offer convenience and efficiency for the customer—it only takes 0.3 seconds to approve a loan application.”

Distinct market structures, regulatory environments and customer needs have led to a wide variety of digital lending models, Punatar believes. There is the complexity of the digital lending ecosystem in its dynamic nature, that makes strict categorisation difficult, but generally, she identifies seven primary digital lending models:

• Online lenders. Full end-to-end digital lending products online or via mobile applications. Examples include Lidya, Branch, and Tala , who help entrepreneurs access funding in emerging markets, including Nigeria, Kenya, and the Philippines.

• P2P platforms. Purely digital platforms that match a borrower with an institutional or individual lender and facilitate the digital transaction. In this model, P2P lenders like CreditEase and KwikCash often design the product, score the borrower, and may support repayment and collection processes.

• E-commerce and social platforms. These are digital platforms where credit is not their core business, but they leverage their digital distribution, strong brand, and rich customer data to offer credit products to their customer base – such as Amazon and WeChat.

• Marketplace platforms. Marketplaces, like Loan Frame in India, are digital platforms who use proprietary algorithms to match a borrower with the right lender. Once funds are dispersed, the customer relationship is direct with the lender.

• Supply chain lender. Firms such as Tienda Pago and M-Kopa Solar provide digital short-term working capital loans for microenterprises to purchase inventory from their distributors, or for pay-as-yougo financing of an asset purchase. The distribution network enforces repayment through penalties if necessary. For example, suppliers might withhold deliveries of goods or turn off utilities in the case of late payment.

• Mobile money lenders. Firms such as Kopo Kopo partner with mobile network operators to offer mobile money loans to their customer base, leveraging mobile phone data for credit scoring. In this model, physical agent networks where customers can go to complete cash-in / cash-out transactions supplement the digital interface of the mobile phone.

• Tech-enabled lenders. These are traditional lenders (like Aye Finance in India and Accion Microfinance Bank in Nigeria) providing a ‘tech and touch’ approach.

Digital lenders to disrupt predominant banking system

Lending has moved away from being a banking only service and has expanded into a number of other industries. “Companies like Amazon and WeChat are now using vast amounts of customer data to provide faster loans to their customers. This, along with the changes brought in by digital only banks and P2P lending platforms, means that the whole digital lending ecosystem is wide open for new and innovative solutions,” Dan Jones, Partner and Head of UK Digital at Capco, says.

Year-on-year, peer-to-peer lending continues to grow and have a strong impact across all markets. The growth demonstrates that more lenders and borrowers believe the industry to be a real alternative to traditional lenders.

The P2PFA figures also show a growth in users of peer-to-peer lending. In the past 12 months, the number of lenders increased by more than a fifth (22 percent) to just over 128,000, while borrowers have almost doubled (96 percent) to 273,000. Goldman Sachs predicts that almost $11 billion of bank profits from lending will move to the new start-up social economy by 2020—about 5 percent of the current market. There is no doubt digital lending marketplaces are disrupting the predominant banking model.

A good example of this disruption is the case of fintech company Zopa. By loan volume, the company is the largest peer-to-peer lender in the UK. Today, the company’s website states that it has lent more than £2.38 billion to UK consumers.

For more on digital lending read, The Potential of Digital Lending

Digital lending challenges

Risks are present in any lending process and there are three subsequent challenges to consider. “Minimising risk means spotting deviations in expected behaviour of the loans on book as early as possible and being able to act on this information”, Xavier Fernandes, analytics director at Metapraxis, says. To minimise risks, it is important to understand what is statistically significant in a loan’s performance, and then be able to identify and quantify the appropriate action to apply to new loans.

Modern AI techniques can be applied to predict the loan outcomes even after just a few months on book, which makes the digital lending market much more agile. “Optimising pricing to complement both risk management and the competitive landscape will attract the right number of customers within the right risk appetite. AI technologies are essential in achieving this, and savvy lenders need to strike the right balance between pricing to manage risk and the competitive environment to ensure they perform well. Blockchain also can help. By improving the traceability of data connecting to any one credit score, it will be easier to make and review any decisions should the loan deviate from its expected behaviour. This undoubtedly helps to optimise credit score models. However, application of blockchain will expose businesses to risks, such as data confidentiality and legal liability of smart contracts, so they will need to be prepared for these,” Fernandes believes.

Digital lending isn’t just about having the data; it’s about understanding and leveraging it correctly. “A clear understanding of the status of a loan or a customer at each stage of its lifecycle is desirable to maximise machine learning algorithms’ accuracy when predicting what will happen to any new customer or loan with similar characteristics. The more lifecycles of loans and customers that firms have data for, the better their algorithms and future predictions will be. This is at the heart of maximising analysis insight in the digital lending market,” an analytics director at Metapraxis explains. Importantly though, digital lenders shouldn’t wait until they have a perfect set of data. Starting with the data inputs they do have, applying algorithms and then identifying which input metrics could improve the algorithm by being of better quality is the best way to ensure speed to value from the data management process.

Jon Hall, Managing Director of Masthaven Bank, also notes that blockchain can help in delivering a ‘personal finance passport’ that can unlock verification and decisioning. “Advanced technology in this space is sorely needed. At the moment, basic algorithmic credit scoring models are restricting potential responsible borrowers from affordable finance options because the technology is inflexible to an individuals’ needs. The mortgage and lending industry needs new technology that can match the same quality and fairness that manually underwritten products provide. Blockchain may be the first step towards a fairer model”. According to Hall, the biggest challenges forthe digital lending market include customer identity verified on mobile devices, personalised affordability and holistic and integrated income verification.

The future

Innovation and market expectations will continue to alter and refine the digital lending landscape. Key players will continue to test, refine, and evolve their business models and value propositions based on customer needs and market experience. However, the similarities shared by today’s successful models are likely to remain prominent, Priya Punatar believes: “Advanced digital lenders have leapfrogged over traditional lenders to provide customers with a faster, more transparent, and convenient service. Traditional banks will have to give customers similar benefits if they hope to compete.”

The digital lending industry is facing a number of challenges. As an example, data management and credit score models’ require improvements. As Rob Moffat, Partner at Balderton Capital, the leading early stage VC focused on Europe, says, AI & ML can help in data management. He believes, the winners will be the companies with the largest, freshest and cleanest data to work with.

A huge amount of consumer and SME data is now available through Open Banking, and data management is now more essential in loan practices than ever. “Big data comes with big processing! An intelligent data management can alleviate heavy processes from platforms, removing the need for timely data replication and processing – instead allowing for machine learning and AI to be performed in real time. In both ML and AI, great progress has been made in automated expense and asset classification. This gives businesses a much more informed idea of their clients’ risk profile, the trend has shown greater loan approvals as a more comprehensive scope of data is considered. With regards to what can ML and AI can do for clients, automated insights can be provided to help consumers repay their loans and meet their targets faster and easier as their financial positions change,” Capco’s Dan Jones says.

Regulation is another challenge, Capco’s experts argue. The rise of new players in the market and the types of lending products being offered drives a need for more rigorous regulation being brought in to place to protect customers.